IRS Notice CP45: What It Is and What to Do

IRS Notice CP45 is a notice that the IRS sends to a taxpayer to inform them that the IRS was unable to comply with the taxpayer’s request to apply their overpayment from the tax return for one tax year to the subsequent tax year.

This typically occurs when the taxpayer files a tax return, indicating on that tax return that they want the overpayment applied to their liability for the next year, but the three-year refund statute expiration had expired before the return was filed.

Here is a redacted Notice CP45 that the IRS sent one of our clients.

Table of Contents

IRS Notice CP45 At a Glance

| Notice Type: | Informational |

| Generated By: | IRS IMF |

| Preceded By: | Late-Filed Tax Return Filing (Typically) |

| Followed By: | N/A |

| Recommended Action: | Ensure Accuracy of Notice |

IRS Notice CP45 Explained, Part by Part

Here is a full explanation of the Notice CP45, part by part.

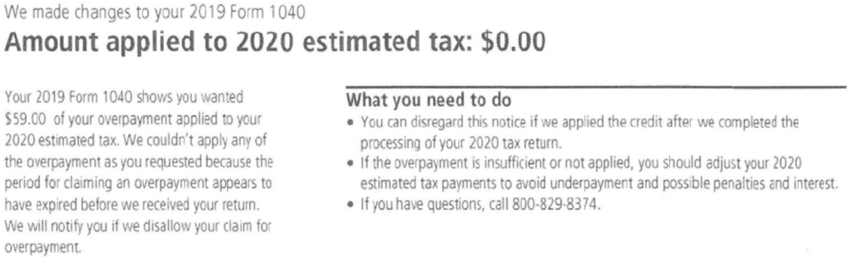

Part 1: Amount of Overpayment Applied

At the beginning of Notice CP45, the IRS informs you how much of your overpayment from the tax return you filed that you wanted to be applied to another year it actually applied to that year.

In many cases, this amount is zero because the refund statute expired for the overpaid year.

The IRS communicated this to our client with this language on the CP45 Notice:

“We couldn’t apply any of the overpayment as you requested because the period for claiming an overpayment appears to have expired before we received your return.”

Part 2: Additional Information

Next, the IRS provides some additional information, such as:

- The official IRS webpage for the CP45 Notice

- Where to obtain tax forms, instructions, and publications

- That you can pay your federal taxes online at www.irs.gov/payments

- Where and how to contact the IRS by mail concerning this issue

- That you should keep the Notice CP45 you received for your records

Free Consultation

Got a CP45 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhy the IRS Sends Notice CP45

The IRS sends Notice CP45 to inform you that it has reduced — often to zero — the amount of an overpayment for one tax year that you elected to have applied to another — typically the following — tax year.

What You Should Do If You Receive a Notice CP45

If you’ve received Notice CP45, here is what you should do (step by step).

Step 1: Determine if the IRS’s determination is correct.

There are a variety of reasons why the IRS may have adjusted the application of your overpayment, so read the IRS’s reasoning at the top of the notice to understand the particular reason why it adjusted your overpayment application.

For example, in this redacted Notice CP45, the IRS states its reason it did not apply the overpayment is “because the period for claiming an overpayment appears to have expired before [they] received [the] return.”

Whatever the IRS’s reason is, make sure you understand it so that you can determine for yourself if the IRS is correct or not.

Step 2: Correct any errors with the IRS.

If the IRS did make a mistake and credited to the other year less than it should have, bring it up to them.

It’s not uncommon for the IRS to, say, not give you credit for the extension you filed for the year, which would extend the amount of time you had to claim a refund or apply an overpayment for that year.

If you think the IRS made a mistake, call the phone number in the “What you need to do” section of the notice.

Step 3: Deal with the year for which you owe.

Finally, you have to figure out what to do with the amount you owe the IRS after you’ve cleared up any disagreements with them concerning the amount as well as obtained any possible penalty relief for your account.

You can, of course, pay off your balance in full.

This will (obviously) stop future penalties and interest from accruing.

However, a better option — if you qualify for it — is an offer in compromise.

An offer in compromise is an agreement you make with the IRS in which the IRS agrees to accept a lower amount to satisfy your tax debt than you actually owe.

That said, not all taxpayers qualify for an offer in compromise, so there are other options, such as a temporary hardship placement called currently not collectible status as well as installment agreements for taxpayers who wish to pay their balance over time.

For an overview of how tax relief works, read our article What Is Tax Relief and How Does It Work?.

“Working with Luke at Choice Tax Relief has been a fantastic experience. His commitment to clear communication is what truly sets him apart. I was always impressed by his responsiveness to my questions, and his consistent, proactive updates.”

Get Help Now

Got a CP45 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.