IRS Notice LT14: The IRS Isn’t Letting You Forget About Your Balance

IRS Notice LT14 is the “You Have Past Due Taxes” notice the IRS sends to a taxpayer to inform them that their outstanding balance is still unpaid.

This notice is not a direct threat of levy, but it is a signal that the IRS is moving you through collections.

So if you ignore your unpaid balance altogether, the IRS may utilize its collections authority to collect your outstanding balance from you via tools such as bank levy or wage garnishment.

Here is a redacted Notice LT14 that the IRS sent to one of our clients.

Table of Contents

IRS Notice LT14 At a Glance

| Official Name: | "You Have Past Due Taxes" Letter |

| Notice Type: | Reminder or Contact Attempt |

| Generated By: | IRS ACS Support |

| Preceded By: | Various |

| Recommended Action: | Pay Your Balance or Enter Into Resolution |

| IRM Reference | IRM 5.19.5: ACS Inventory |

IRS Notice LT14 Explained, Part by Part

Here is a full explanation of the Notice LT14, part by part.

Part 1: Notice of Unpaid Balance

First, the IRS directly informs you that you “still” have an unpaid balance with them.

If you have them the victim of a federally declared disaster such as a fire, flood, hurricane, or other naturally occurring environmental disasters, then the IRS may offer additional aid.

The IRS goes in-depth with their disaster care on their website; otherwise, the window of time to take action is still extremely narrow.

Part 2: What the IRS Says You Need to Do

Next, the IRS will tell you what you “need” to do — which is more like what they want you to do.

Since the IRS is notifying you of your outstanding balance, the government obviously wants you to pay off your balance immediately.

You can either use the provided payment coupon via check or money order, or pay online at their provided website.

If you cannot pay in full right away, the IRS offers a way to pay your remaining balance if you are up to date on all your filing obligations.

The IRS offers payment plan options that you can apply for in order to pay off your balance over time.

If you cannot pay due to financial hardship, then the IRS can possibly delay collection until your situation improves a bit.

Again, this is given on a case-by-case basis.

If you have more questions about your LT14 notice, the IRS also provides a website.

We’ve helpfully linked it here.

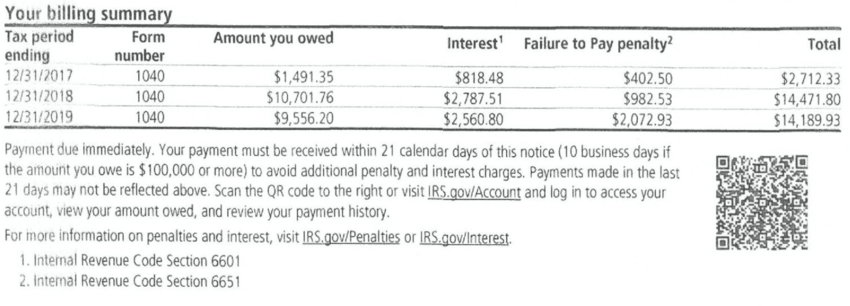

Part 3: Billing Summary

Then, the IRS gives you a table of your billing summary.

It will have the specific tax period, form number, amount owed, interest penalties, and failure penalties.

Each line will be for the respective period, and what you owe is the total of all of them.

Your payment will be due within 21 calendar days of the notice.

However, if you owe more than $100,000, you will only have 10 business days to pay back your balance.

If you wait more than the provided time periods, then you will incur more interest and other penalties against your balance.

If you’ve made a payment in the last 21 days (from the date of the notice), then the payment will likely not show up on the letter.

Consult your online account for more updated information.

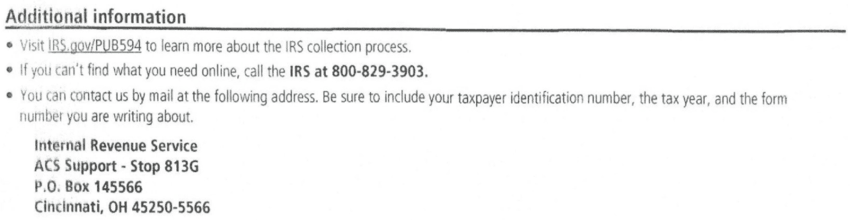

Part 4: Additional Information

Then, the IRS will provide you with additional information.

If you have questions, it has provided you with a phone number you’re able to contact.

If you cannot find everything online and calling them isn’t working, then you can mail the IRS questions or corrections.

If you choose to mail the IRS anything, it’s important that you do not forget to include your TIN, tax year, and the form that you’re contacting them about.

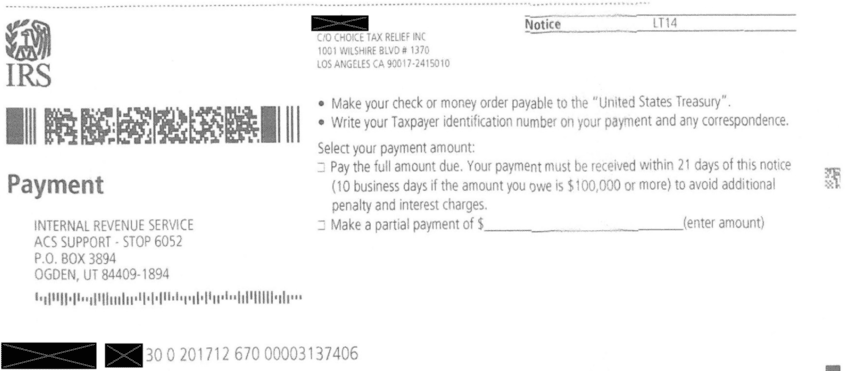

Part 5: Payment Coupon

Lastly, the IRS will provide you with a payment coupon.

You send this in with your check or money order (made payable to the United States Treasury).

Do not forget to check the box for what you’re paying.

If it’s the full amount, then be sure it’s within 21 days of the notice (or 10 if you owe more than $100,000).

If it’s the partial amount, don’t forget to fill in how much you’re paying.

No matter how much you’re paying, don’t forget to include your TIN on your payment and any other correspondence you have with the IRS.

Free Consultation

Got a LT14 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhat You Should Do If You Receive an LT14

Below are steps for you to take after you receive an LT14 Notice from the IRS.

Step 1: Follow Up If You Think There Was A Mistake

If you believe there is an issue with your balance, contact the IRS sooner rather than later.

Your balance is your responsibility, and if the IRS presents you with a discrepancy, you have the right to protect it.

You should always double-check to make sure the IRS hasn’t made an error on your account.

It isn’t a flawless system and is still capable of error.

It’s up to you to make sure everything is done correctly.

Is there still a balance, or has the IRS not processed your payment?

Is there any other possibility of error?

If you find an error, then contact the IRS as soon as you can.

It likely won’t be an easy process, but it’s very necessary to protect your money and your account.

You will need to hurry since there is only a 21-day period for you to dispute the charges before the IRS takes any more action.

Since it’s difficult and annoying, Choice Tax Relief offers this service to our clients.

Step 1a: Follow Up If You Qualify For Disaster Relief

If you are a victim of a disaster, like fires, floods, etc., then read up on the IRS’s disaster policies.

There may be more leniency on deadlines or payments depending on the severity of your situation.

Make sure you’re up to date on the latest policies, and remember to prioritize your safety.

The IRS has policies in place to allow you to think about your safety first, and bills second.

Step 2: Pay Off Your Balance

If you haven’t found any errors, then you should pay off your balance as soon as you can in order to ensure the IRS doesn’t take more drastic measures.

While it appears to be a painfully obvious solution, it’s reliable and effective when it comes down to it.

Payment in full will halt any IRS threats and actions, alongside alleviating any current actions the IRS is in the process of taking.

Step 3: If You Cannot Pay Off Your Balance

If you cannot afford to pay off your balance, then you can apply for an Offer In Compromise (OIC).

The OIC is a highly effective agreement between the taxpayer and the IRS to settle tax debts for less than the original cost. It may not be guaranteed, but it’s always worth a shot to try and apply.

If the OIC isn’t a feasible option, then consider applying for a temporary hardship placement (called currently not collectible status).

That will halt the IRS from taking any action for a predetermined period of time.

During this time, you are expected to save and prepare to pay off your debts.

It will simply buy you some time, away from the IRS push and pull.

“I interacted with 4 other providers before finding Choice Tax Relief. All the others were offering a “let’s get your money up front, then see how this all plays out for you” approach.”

Get Help Now

Got a LT14 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.