Offer in Compromise Example: How We Settled $77,478 For $5,273

If you’re wondering what the offer in compromise process actually looks like, then this is the article for you.

In the next few minutes, I’m going to walk you through a real offer in compromise example — an actual submission that we made on behalf of our client that was accepted by the IRS and saved our client over $70,000 in tax debt.

Names have been changed to protect the identity of our clients.

Want more offer in compromise stories?

Check out our list of offer in compromise success stories!

Offer in Compromise Example: $77,478 Settled For $5,273

Our client — let’s call her Carol — came to us owing $77,478.48 in IRS back taxes.

She had racked up this tax debt over the better part of the last decade.

Based on a review of Carol’s financial situation, our legal team quickly concluded that she would be a great candidate for the IRS offer in compromise program.

Although Carol owed almost $80,000 in tax debt, our tax attorneys concluded that she could likely qualify for a settlement amount for less than 10% of that amount.

Carol’s Offer in Compromise Package

So we quickly got to work and prepared Carol’s offer in compromise package, including:

- Our cover letter

- A check from Carol for the $205 filing fee

- A check from Carol for the $40 down payment

- Form 656, completed by us and signed by Carol

- Form 433-A (OIC), completed by us and signed by Carol

- Carol’s most recent paystub

- Carol’s last three months of bank statements

- A Kelley Blue Book estimate of the value of Carol’s car (a 2007 Ford Focus)

- A screenshot of Carol’s retirement account

A Closer Look at Carol’s Form 433-A (OIC)

The Form 433-A (OIC) is the IRS form on which an offer in compromise candidate presents their financial situation and calculates their reasonable collection potential — the amount of money the IRS could “reasonably” expect to “collect” from the taxpayer — which in most cases is the amount that the taxpayer should offer to the IRS.

You can click the image above to see Carol’s entire redacted Form 433-A (OIC), and below I have gone over key aspects of Carol’s form, including the vehicles section.

Vehicles

Like most of a taxpayer’s assets, a taxpayer’s equity in their vehicles are fair game for an offer in compromise.

However, there are some taxpayer-friendly calculations that you need to make when calculating just how much your vehicle counts against you for offer in compromise purposes.

Carol’s only asset of note was her paid-off 2007 Ford Focus, which Kelley Blue Book indicated had a fair market value of $1,663.

IRS collections guidelines allow one to value most of their assets at an 80% quick-sale value, which would make the quick-sale value of the Ford Focus $1,330.

But wait — you can also subtract $3,450 from this amount to determine (not below zero) the amount of equity in your vehicle you must include in your offer.

In this case, because $3,450 is greater than $1,330, we didn’t have to include any of Carol’s equity in her vehicle in her reasonable collection potential for offer in compromise purposes!

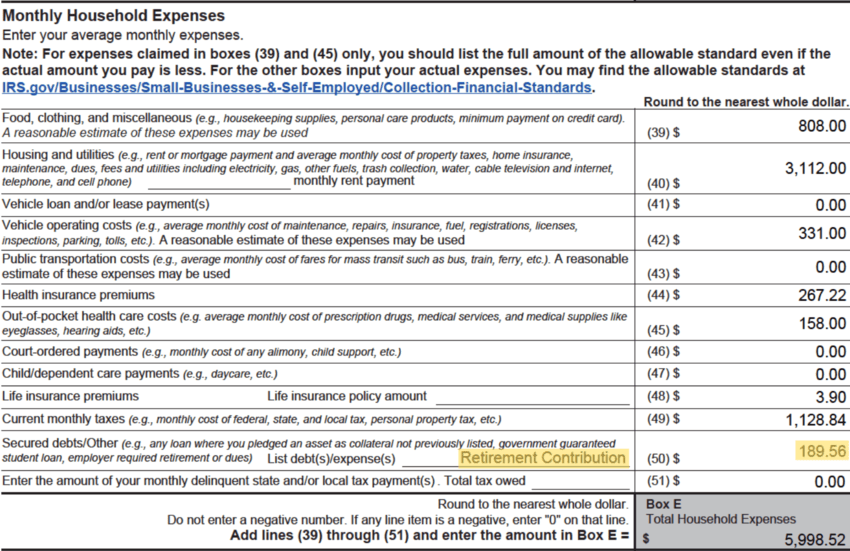

Retirement Contributions Expense

Now let’s take a look at Carol’s monthly household expenses calculation.

In general, we want to beef these expenses up as much as possible — I’m not saying that we make numbers up, but that if there’s a “grey” area of whether a certain expense should be indicated on here, we include it so as not to do the IRS’s work for them.

Generally, retirement account contributions are voluntary and are therefore not allowed as an expense against monthly income in calculating a client’s monthly disposable income; the IRS believes you should be paying them off first before contributing to your 401(k).

However, in Carol’s case, we determined that her retirement contributions were required as a condition of employment as a government employee, and we included them in our calculation.

A Closer Look at Carol’s Form 656

Carol’s Form 656 was fairly standard: she didn’t qualify for low-income certification, she did not have to report any business information, and she was applying for the most commonly offered and accepted type of offer in compromise — the doubt as to collectibility offer.

Payment Terms

I will draw your attention, however, to Section 4 of the Form 656: Payment Terms.

You’ll notice that Carol is submitting a “Lump Sum” offer in compromise — one that she will pay off within five or fewer months from the date the IRS accepts her offer.

In the table shown, you will note the following:

- Carol’s $5,417.20 offer amount, as calculated on her Form 433-A (OIC).

- Her 20% down payment of $1,055.64 (she must submit a 20% down payment with her lump sum offer because she does not qualify for low-income certification)

- Her remaining balance of $4,361.56, that she indicates she will pay within five months after offer acceptance.

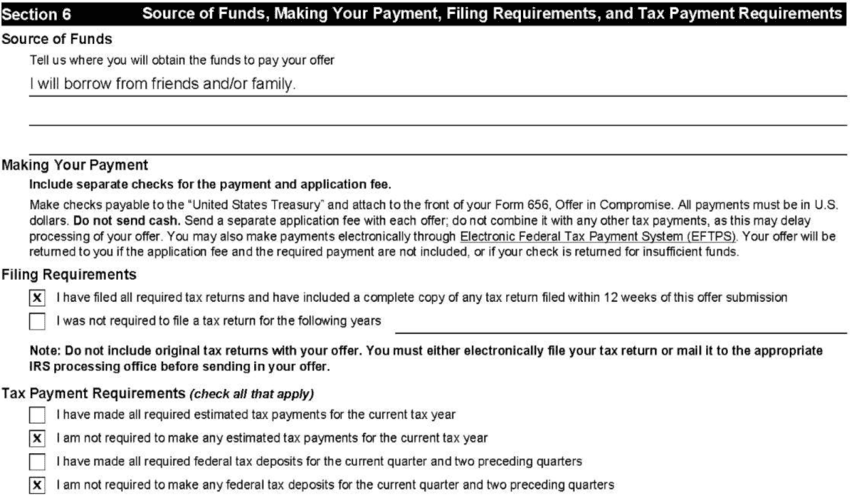

Source of Funds and Other Offer in Compromise Requirements

In Section 6 of the Form 656, the IRS inquires how you intend to pay the funds for your settlement offer — and sometimes it managers to trap ignorant taxpayers with this line.

I’ve seen some self-prepared offers in compromise in which the taxpayer wrote, “I will be paying my offer in compromise from my $100,000 savings account” — but they didn’t disclose this $100,000 savings account on their Form 433-A (OIC)!

It should be no surprise that the IRS rejected their offer in compromise!

You’ll also notice the additional requirements when submitting an offer in compromise:

- You must have filed all required tax returns and have included a complete copy of any tax return filed within 12 weeks of when you submit your offer in compromise.

- You must have made all required estimated tax payments for the current tax year.

- You must have made all required federal tax deposits for the current quarter and two preceding quarters.

If you were not required to file such returns or make such payments, you must check the appropriate box(es).

Good News: Offer Accepted!

In early June, we received a letter from the IRS Offer in Compromise Unit that began with the words we like to see:

“We have accepted the offer in compromise you signed and dated on 3/17/2025. The acceptance date is the date of this letter and acceptance is subject to the terms and conditions on the enclosed Form 656, Offer in Compromise.”

Woohoo!

We had saved Carol thousands of dollars!

Free Consultation

Owe the IRS? Don’t wait for their next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXGet Help Now

Owe the IRS? Don’t wait for their next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.