Offer in Compromise Success Stories

Although the IRS rejects the majority of offer in compromise submissions it receives, we’ve had a nearly 100% success rate with our offer in compromise submissions, and we are pleased to share some of the amazing results we’ve achieved for our clients below.

Names have been changed to protect the identity of our clients.

Want to learn more about the offer in compromise process?

Check out our article on offer in compromise examples, where we take you through the actual forms, documentation, and processes that go into a successful offer in compromise submission.

Offer in Compromise Success Story #1: $89,189 Settled For $2,097

Taxpayer’s Location: Brooklyn, New York

Taxpayer’s Original Debt: $89,189

Taxpayer’s Settled Debt: $2,097

Our first offer in compromise success story comes from an individual — let’s call him “Cooper” — who owed $89,189 to the IRS for tax years 2013-2017.

What’s interesting about this individual is that he:

- Had an income in excess of $200,000 per year

- Had previously submitted an offer in compromise through another company back in 2018 that got rejected

So these two things would obviously make it an uphill battle for us to get Cooper’s offer in compromise accepted, and it was an uphill battle that lasted — from our initial contact with Cooper all the way through our negotiations with the IRS and finally to offer in compromise acceptance — over a year and a half.

Our initial offer was rejected; so we had to appeal that rejection; and that’s why it took a bit longer than most offers to get approved.

I will now take you through our journey with Cooper’s offer in compromise, including the appeal, so that you can understand what an offer in compromise looks like, from soup to nuts.

Initial Situation: $89,189 Owed

Here’s this individual’s initial email to us:

At this point, we got on the phone with Cooper to determine that he could actually qualify for an offer in compromise, taking him through the financial analysis that I have discussed at length in this article on the offer in compromise formula.

We did not know for sure whether Cooper would qualify, especially with his high income and the fact that he had fairly recently submitted an offer in compromise that was rejected, and we let Cooper know that:

- we were going to get him in the best possible resolution with the IRS that we could

- we thought he had a fairly good chance of getting an offer in compromise accepted, and we would appeal any rejection, but that

- he should prepare for the fact that maybe at the end of it the best we could do is place him into an installment agreement because offers in compromise are far from guaranteed, especially given Cooper’s high income and previous offer in compromise rejection

Cooper understood, and he retained us to represent him before the IRS in this matter to get him into a resolution.

Initial Offer in Compromise Submission

So the reason why Cooper had any chance at an offer in compromise on $90,000 of tax debt with a $200,000 income is because:

- Cooper lived in Brooklyn in New York City — this helped him because for certain expenses such as your housing expenses and your vehicle operating expenses the IRS allows you to claim higher amounts for those expenses (to the extent they’re actually paid) in high cost of living areas, and Brooklyn is one of the highest cost of living areas in the country

- Cooper had several dependents living with him in Brooklyn, New York, who were not earning income themselves and depended on his income to survive; these individuals included Cooper’s wife, mother-in-law, and several children. I believe he had three or four dependents in total that we ended up claiming on his offer in compromise paperwork.

So we gathered all this information from Cooper about his financial information and put it on a Form 433-A (OIC).

Receipt of the Processability Letter

Since our offer was prepared correctly, and a down payment was attached, the IRS deemed our offer processable and sent the taxpayer a processability letter, signed by the process examiner who reviewed the offer, reading as follows:

“We received your Offer in Compromise.

You will be contacted by 3/11/2023.

If you receive collection notices while your offer is pending, please contact the number on this letter.

“While investigating your offer, we will determine whether a notice of federal tax lien should be filed in order to protect the government’s interests.

If you disagree, you may ask the Service not to file the notice of federal tax lien.

Please read the enclosed publications regarding the types of appeal available.

If we determine to file a notice of federal tax lien we will provide you with notification within five days of the filing.

You will have the opportunity to request a hearing with Appeals at which you may propose alternative methods for protecting the government’s interest.

“If you receive collection notices while your offer is pending, contact the number on this letter.

“If you have nay questions, please contact the person whose name and telephone number are shown in the upper right hand corner of this letter.”

This letter does not mean the IRS has accepted the offer in compromise; it simply means that the IRS has deemed it processable and able to be reviewed by an offer examiner or an offer specialist.

Receipt of the Letter 6120C

After receiving the processability letter, we didn’t hear anything from the IRS regarding this offer for some time — of course, this was completely expected given how long offers in compromise take.

But a little after four months after submitting the offer, we received the Letter 6120C from the Brookhaven IRS Center Centralized Offer in Compromise Unit in Holtsville, NY.

You can click here to read the entire letter, but here’s the gist:

- An IRS offer examiner would contact us within 90 days from the date of the letter with their decision on the offer

- The IRS has suspended taking collection action against the taxpayer while it evaluates the offer we submitted

- If we had submitted a periodic payment offer in compromise — which we did not — the taxpayer would be required to continue to make monthly payments while the IRS considers the offer

- The taxpayer is required to continue to file and pay their taxes on time while the IRS is reviewing the offer (this includes estimated tax payments and federal tax deposits)

Offer in Compromise Transferred to the Field

A few weeks after sending the Letter 6120C, the IRS sent us a letter informing us that the offer had been transferred to the IRS field office in Savannah, Georgia.

On this letter we learned the name of the offer specialist that would review and make a decision on the offer — D. Clegg — who the letter informed us would contact us within the next 45 days.

Although we don’t always know exactly why an offer is transferred from the Central Offer in Compromise (COIC) office the offer was initially sent to to a Field Offer in Compromise (FOIC) office, we do know that offers that the IRS deems as “more complex” are transferred to an FOIC.

IRS’s Preliminary Conclusion to Reject

Some time later, Leah McLaughlin, the enrolled agent in my office working the case, was contacted by the IRS offer specialist, D. Clegg.

Ms. Clegg informed Leah that she was proposing to reject the offer, communicating to her that she is proposing a monthly installment agreement of $2,108 instead.

Ms. Clegg sent Leah her Income/Expense Table (IET) and Asset/Equity Table (AET), showing her calculation of Cooper’s ability to pay.

Note that this faxed correspondence was dated in late July, and this commenced a five-month battle between my office and the IRS offer specialist.

In our mind, by this point, the client clearly qualified for an offer in compromise, and we made this argument to the IRS offer specialist every which way.

Nevertheless, the IRS offer specialist and her manager issued a rejection letter in December.

IRS’s Offer in Compromise Rejection Letter

In December, the IRS offer specialist and her manager sent us a copy of the letter they sent the taxpayer rejecting the offer in compromise.

Along with the rejection letter, they also provided their Income/Expense Table and Asset/Equity Table showing what they believe Mr. Cooper could pay.

The assets and equity weren’t really a problem; however the IRS’s calculation of Mr. Cooper’s disposable income on their Income/Expense Table was much higher than our calculation of his disposable income.

| Gross Wages | $17,450 | $15,984 |

| Food, Clothing, & Miscellaneous | ($2,244) | ($1,993) |

| Housing and Utilities | ($2,661) | ($0) |

| Vehicle Loan and/or Lease Payment(s) | ($827) | ($629) |

| Vehicle Operating Costs | ($406) | ($379) |

| Public Transportation Costs | ($242) | ($242) |

| Health Insurance Premiums | ($282) | ($0) |

| Out-of-Pocket Health Care Costs | ($375) | ($319) |

| Court-Ordered Payments | ($991) | ($0) |

| Child/Dependent Care Payments | ($4,000) | ($4,000) |

| Current Monthly Taxes | ($5,492) | ($6,086) |

| Total Household Expenses | ($17,520) | ($13,648) |

| Remaining Monthly Income | $0 | $2,336 |

The IRS’s offer specialist and her manager were clearly either asleep at the wheel or had no idea how offers in compromise work because:

- They disallowed the taxpayer’s housing expenses, despite us providing the offer specialist with credit card statements showing the lease payment as well as the taxpayer’s lease agreement

- They did not give credit to the number of people in the taxpayer’s household for the taxpayer’s new child, despite the fact that we provided to the offer specialist information regarding the child, including Social Security number

- They disallowed the taxpayer’s child support payment, despite it being court ordered and us providing the offer specialist with the court order

There were some other things wrong as well, but we basically knew at this point that we were dealing with idiots at the IRS — no surprises there; it’s not like the IRS hires the best and the brightest — and we naturally decided to appeal the rejection.

Our Appeal of the Offer in Compromise Rejection

On December 28 — before the 30-day deadline to appeal the offer in compromise rejection — we faxed our Form 13711 “Request for Appeal of Offer in Compromise” to the fax number on the offer in compromise rejection letter.

Here is a list of all our disagreed items on the Form 13711, which formed the basis of our appeal:

| National Standard | The household contains a total of six people. The 2022 tax return and the birth certificate for the child born in 2023 are attached. Please increase to $2,705. |

| Housing and Utilities | No amount was allowed for housing and utilities. Please increase the expense to $3,229. A copy of the lease and credit card statements that show proof of payment for housing and utilities are attached. |

| Court-Ordered Payments | Taxpayer is required to pay court-ordered child support of $991. A copy of the court order and proof of payment are attached. |

| Out-of-Pocket Healthcare | Please increase to $474 to allow for six people. |

| Bank Accounts | The taxpayer has $3,097 in their checking account, and his allowable living expenses are in excess of this amount. Therefore, no amount should be indicated on the AET. |

Further Negotiations With an Amended Offer

Within a couple months, our enrolled agent Leah had negotiated a final offer amount with the IRS of $2,097 and submitted an amended offer to the offer specialist using Form 656.

Offer in Compromise Acceptance in the Amount of $2,097!

Then, in late March, we received this envelope at our office:

Inside, was an offer in compromise acceptance letter!

Free Consultation

Owe the IRS? Don’t wait for their next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXOffer in Compromise Success Story #2: $10,447 Settled For $200

Taxpayer’s Location: Spokane, Washington

Taxpayer’s Original Debt: $10,447

Taxpayer’s Settled Debt: $200

“Tom” came to us with a relatively small tax debt of $10,447.

Now, the IRS tried to return this offer to us as unable to be processed — but we were able to shut this argument down and get the offer pushed through (more on that later).

Initial Offer in Compromise Submission

On September 11, we submitted our offer in compromise for Tom.

Because Tom qualified for the low-income certification, he did not need to submit any down payment or application fee in the offer package.

Our 433-A (OIC) was fairly straightforward, reporting only $11.17 in cash in a credit union account and a 2012 GMC Sierra with 200,000 miles on it and a fair market value of $4,465; after running some calculations in favor of the taxpayer, we reported only $122 in assets includible in the taxpayer’s offer amount.

As far as income was concerned, we only reported Tom’s monthly disability benefit of $450 per month; the national standard for food, clothing, and other miscellaneous items alone eliminated this amount, leaving Tom with no monthly disposable income for offer in compromise purposes.

Therefore, we rounded up the available assets of $122 to $200 for an even offer amount.

Offer in Compromise Recommended for Acceptance

Then, on January 30, our tax attorney Andrea Coins received a fax from our client’s offer examiner with the following message:

“I received all the requested information for Mr. Tom. The offer is being recommended as an acceptance. Have a nice day!”

We were thrilled and told our client!

Of course, this fax was just an informal notification from the offer examiner; we still had to receive the official offer in compromise acceptance letter from the Centralized Offer in Compromise Unit.

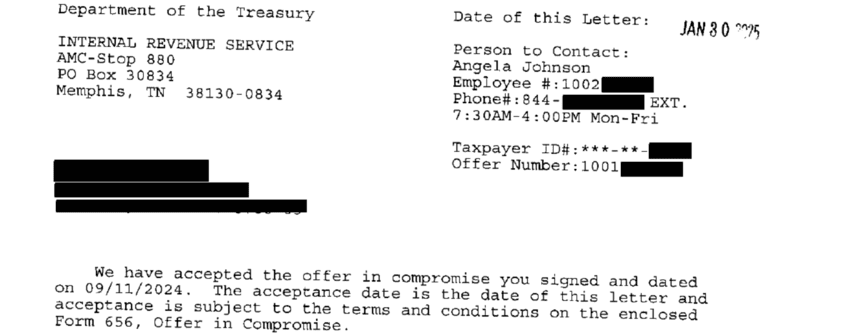

Offer in Compromise Acceptance Letter

And that letter came in the mail shortly thereafter with these words:

“We have accepted the offer in compromise you signed and dated on 9/11/2024.”

We were thrilled to share the news with our client that we had successfully settled his $10,447 of tax debt for only $200!

Get Help Now

Owe the IRS? Don’t wait for their next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.