IRS Notice CP523H: What To Do When the IRS Threatens to Terminate Your IA

IRS Notice CP523H is the Notice of Intent to Terminate Your Installment Agreement that the IRS sends to a taxpayer when it believes that the taxpayer has defaulted on an installment agreement that includes payment toward a Shared Responsibility Payment (SRP).

The SRP is the amount the taxpayer of the “Obamacare penalty” that the taxpayer owed for one or more tax years between 2014-2018.

This penalty, created by the Affordable Care Act, was imposed on taxpayers who did not have the minimum health coverage essential for themselves and other members of their tax household and who did not qualify for an exemption under Internal Revenue Code Section 5000A.

It was eliminated beginning in tax year 2018 as part of the Tax Cuts & Jobs Act.

The Notice CP523H is year-specific, so if the installment agreement covered multiple years of SRPs, the IRS will send a separate CP523H for each SRP.

Here is a redacted Notice CP523H that the IRS sent one of our clients.

Table of Contents

IRS Notice CP523H At a Glance

| Letter Type: | Notice of Intent to Terminate Installment Agreement |

| Generated By: | IRS Service Center |

| Preceded By: | N/A |

| Followed By: | Collections Activity |

| Recommended Action: | Cure IA Default Condition, Restructure IA, or Seek Alternative Resolution |

IRS Notice CP523H Explained, Part by Part

Here is a full explanation of the Notice CP523H, part by part.

Part 1: Notice of Intent to Terminate Your Installment Agreement and Reason for Potential Termination

First, you’ll see the CP523H Notice open with the IRS telling you what condition of your installment agreement has been defaulted; this reason is generally indicated after the phrase “Notice of intent to terminate your Installment Agreement:”.

For this specific taxpayer, the IRS intends to terminate their installment agreement because their monthly payment is past due.

The reasons on the CP523H Notice may differ if the IRS’s intent to terminate is based on a different factor, such as failure to pay additional federal taxes or failure to provide an updated financial statement when the IRS requested it.

Part 2: What the IRS Says You Need to Do Now

Then, the IRS will inform you of what actions it wants you to take as a result of the notice.

Obviously, if you’ve missed your required installment agreement payment (as our client did), the IRS wants you to pay your past-due amount in full now — this is what the IRS instructed our client to do in the bold letters “Pay your past due amount online now”.

Of course, if you are unable to pay what you owe, you have other options that the IRS doesn’t specify here, such as providing updated financial information to the IRS.

If you can prove to the IRS that you don’t have the means to cure the default condition because it would cause you economic hardship, the IRS may agree to restructure your installment agreement.

This process starts with you providing updated financial information to the IRS, such as by providing them with an updated Form 433-F — more on this later in this article.

Part 3: What the IRS Says You Need to Know

In the next section, the IRS informs you of the things that it believes you “need to know” about your situation with them.

First, it explains that your installment agreement covered — likely in addition to other liabilities, such as for regular income tax, interest, and other penalties — an SRP and that you owed an SRP because you did not have the minimum essential health coverage required by the Affordable Care Act.

This section goes on to explain, in three bullet points, the following things:

- that you did not meet the terms of your installment agreement, and as a result, it will be terminated if you do not pay your past due amount within 30 days of the date on the notice

- that the IRS will send you a bill for the full amount you owe the IRS — not only for the SRP but also for everything else you owe the IRS for all tax years — if the IRS terminates your installment agreement and you exhaust your right to appeal the termination

- that interest will continue to accrue on your unpaid SRP balance if you don’t pay the past due amount within 30 days of the notice date

The IRS also informs you that any federal tax refunds indicated on your tax returns may be applied to your SRP balance until it is paid in full.

Note that the IRS can apply your federal tax refunds to all balances, SRP, and non-SRP.

Finally, the IRS informs you that it may reach out to third parties — meaning, people other than you or your authorized representative — to obtain information that it believes is necessary in order to verify information about you and your financial situation and/or to take collection action (such as levy action) against you.

This notice is required by law before the IRS can levy you.

This is because Internal Revenue Code Section 7602(c) requires the IRS to provide you with advance written notice before contacting third parties about your tax debt, and obviously, in serving levy notices to your bank, employer, or other institution, the IRS is contacting third parties about your tax debt.

Note that the IRS may have previously satisfied this advance written notice requirement by sending you a separate notice, such as Notice LT40.

Part 4: Options If You Can’t Pay Your Past Due Amount

The IRS provides several options for you if you cannot afford to pay your debts.

Restructure Your Installment Agreement: Fill out and give the IRS an updated Form 433-F, Collection Information Statement.

Discuss the reason for the defaulted payment with them for a potential agreement to help fix your debt situation.

Consider an Offer in Compromise (OIC): An offer in compromise is a powerful tool allowing you to settle your tax debt for less than you actually owe.

If you qualify, it is one of the best-case scenarios for you as you go about settling your tax debts.

Request a Temporary Collection Delay: The IRS may be able to temporarily delay collections until your situation improves.

It won’t last forever, but it can be enough time to help you get back on your feet.

All three solutions are worth looking into, especially with the help of a tax attorney to help represent you to the IRS.

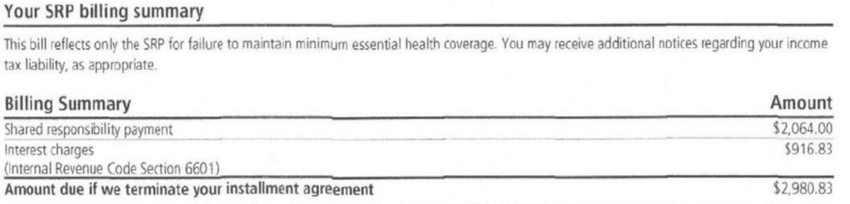

Part 5: Your SRP Billing Summary

Next, the IRS gives you a breakdown of the amount of SRP you owe, along with the interest on it.

The sum of these amounts is the amount that would be due to the IRS (they will bill you for it) upon termination of your installment agreement.

The IRS also reminds you in this section that you may receive additional notices regarding your potentially defaulted installment agreement with respect to your income tax liability; these notices would most likely be sent as Notice CP523.

Part 6: Online Account Access

Then, the IRS will show you how to digitally access your account information.

This can be handy for making payments or checking up on your balance.

While the online portal makes this convenient and easy, it’s always better to keep a paper trail, so make sure you hold onto every hard copy document they send you.

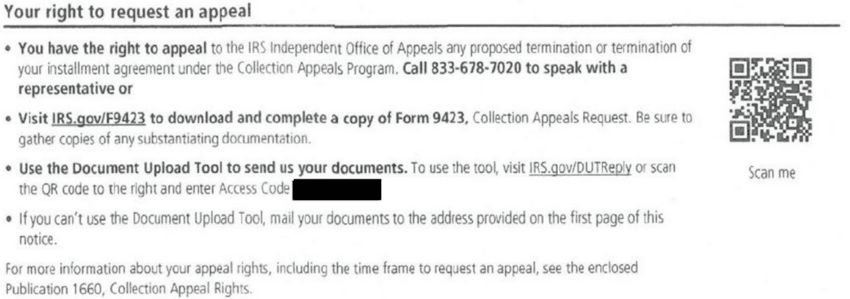

Part 7: Your Right to Request an Appeal

At any point during the process, you may appeal the IRS’s intent to terminate your installment agreement with the IRS’s Independent Office of Appeals.

The process is started by filing a Collection Appeal Request (Form 9423) to the address on top of your CP523H Notice.

An appeal can be an important tool in halting the IRS from terminating your installment program.

Part 8: Where You Can Find More Information

Then, the IRS will provide you with areas where to find more information.

They’ll tell you about your rights as a taxpayer, citing Publication 594 and the IRS Collections Process.

Here are the most important things to note:

- The official IRS webpage for the CP523H Notice

- Where tax forms, instructions, and publications can be obtained

- How to contact the IRS

- That you should keep your CP523H Notice for your records

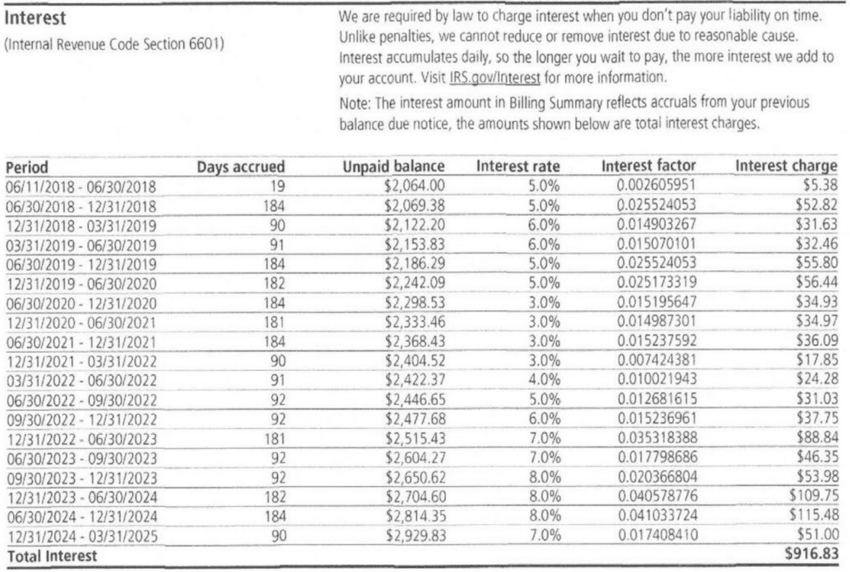

Part 9: Interest

In this section, the IRS breaks down the interest it has charged you since the monthly payment.

Note that IRS interest is compounded daily and subject to change quarterly.

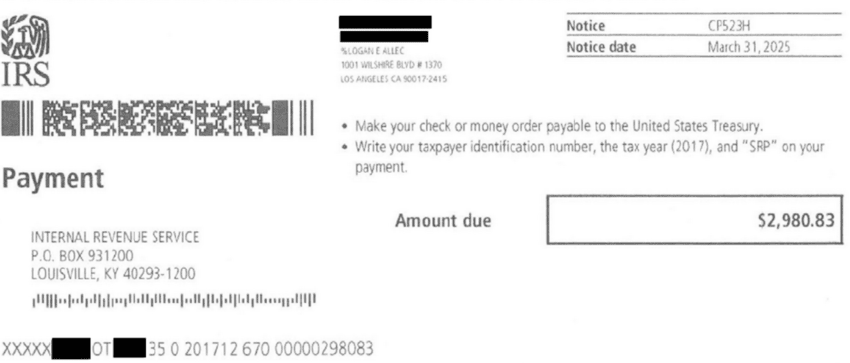

Part 10: Payment Coupon

At the bottom of the CP523 Notice is a payment coupon.

You would submit this with your payment if you intend to fully pay off the amount on your notice.

Free Consultation

Got a CP523H Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhat You Should Do If You Receive a CP523H

Below are steps for you to take after you receive a CP523H Notice from the IRS.

Step 1: Confirm you’ve met the Default Condition

Unsurprisingly, the IRS makes mistakes.

The first step you should take is to make sure the reason the IRS intends to terminate your installment agreement and levy you is true.

If the IRS is saying you haven’t made a monthly payment, take a step back.

Is that true?

Did you make a payment, and they just don’t see or honor it?

If the IRS is saying you update your financial information when they requested it, pause.

Is that true?

Was there no response on your end?

So, read and reread the first part of the CP523 Notice closely.

Note what they’re terminating you for and evaluate the accuracy of their claims.

Step 1a: Dispute the Default Condition if the IRS is Incorrect

Then, if you are certain the IRS is in error because of its reasoning to terminate your agreement, as seen in the CP523H Notice, contact the IRS with their provided phone number and tell them where they’ve made an error.

Most likely, this will not be resolved with a single phone call.

More likely, you’ll explain your position to them and they’ll review your account.

Even though it’s rough, you have a right to do this.

We provide this service for our clients because the IRS does make mistakes when going through the steps to terminate a client when the default conditions haven’t been met.

Step 2: If There Was a Default on your Installment Agreement, Cure It

You will have 30 days from the date of the notice to fix your situation and prevent your agreement from being terminated.

Since it’s from the date the notice was issued, a couple of weeks may’ve already passed.

If there is a genuine default on your agreement, then a payment must be made as quickly as possible.

If the default on your IA is because you missed a monthly payment, then to restate the agreement, you just need to catch up on the payment.

If you’re in default because you gained an additional, new tax debt, then you should pay the bill and contact the IRS after to ensure the original IA is still active.

The most straightforward way, however, is to follow the instructions in the CP523H Notice if you have defaulted.

This will be the most straightforward way to resolve your issue, no matter the given intent to terminate your IA.

If your tax obligations have already been paid and/or you believe that you have not violated your installment agreement, you can call the IRS with their provided number to confirm your account’s current status.

Step 3: If the Default isn’t Cured, Petition the IRS to Restructure the IA OR Seek Alternative Resolutions to your Tax Debt

Sometimes, it’s not possible to catch up on your installment agreement or take the necessary steps to fix your situation.

If you’re at that point, then you need to contact the IRS with their provided number to ask about alternative resolutions or restructure your agreement.

They’ll ask you to submit your updated financial information to prove that your current financial means prevent you from continuing with the present payment solution.

If you want to restructure your IA, we advise you to have a new proposal ready and prepare yourself to negotiate new terms with the IRS.

There’s a possibility of a fee for restructuring, but you can ask about applying to have the fee waived.

Step 4: If You Feel No Progress is Being Made, Consider Filing an Appeal

IRS negotiations and navigations aren’t always easy.

A deadline only adds an additional stress factor.

While we do this for our clients, doing it by yourself is incredibly difficult.

If you’re struggling a lot in restructuring your IA or finding IRS resolutions, remember your ability to make a formal appeal and get your case assessed.

Then, you can appeal through the Collections Appeal Program with a Form 9423 (Collection Appeal Request).

The form gives you the opportunity to appeal if your IA is terminated or if your restructuring request is denied.

The form can be filed before the IRS takes any further enforcement action or after the action has already happened.

Most likely, this is the next step if you fail to respond in time and your current agreement is terminated.

Don’t forget, you’re also allowed and entitled to call a Collections Due Process hearing if your IA is terminated.

You will also subsequently receive a notice of intent to levy.

What Comes After a CP523H Notice?

The notice that comes after a CP523H Notice depends on whether or not you’ve received a notice informing you of your collection due processing hearing rights.

Not sure if the IRS has sent you this notice yet?

Watch the video below!

If the IRS has sent you a CDP Notice

If you’ve previously received a CDP Notice (such as the LT11) from the IRS, your next notice may be a copy of a levy notice sent to your bank or employer from the IRS.

If the IRS has not sent you a CDP Notice

If you haven’t received a CDP Notice, the IRS must send you one before it can take any action to levy you.

Then, an LT11 may follow your CP523H Notice.

How Is This Different From a CP523?

While the CP523 and CP523H are similar notices, the CP523H focuses on the shared responsibility payments concerning healthcare.

The two are similar in most other aspects, stemming from a lack of payment on additional tax or general monthly payments per the IA agreement.

Get Help Now

Got a CP523H Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.