IRS Notice CP63: Why the IRS Is Holding Your Refund

IRS Notice CP63 is the refund hold notice the IRS sends you to notify you that it has processed your recent tax return filing indicating that you are due a refund but the IRS is holding this refund until you take some action, such as filing past-due tax returns.

Here is a redacted Notice CP63 that the IRS sent to one of our clients.

Table of Contents

IRS Notice CP63 At a Glance

| Notice Type: | Refund Hold / Return Delinquency |

| Generated By: | IRS IMF |

| Preceded By: | Filing of Return Showing Refund Due |

| Followed By: | Potential SFR Filing |

| Recommended Action: | File Required Tax Return(s) |

IRS Notice CP63 Explained, Part by Part

Here is a full explanation of the Notice CP63, part by part.

Part 1: Which Refund the IRS Is Holding and Why

At the top of the notice, the IRS tells you exactly which tax year’s refund it’s holding — and why.

For example, in this client’s notice, the IRS is informing the taxpayer in the large, bolded print that it is holding the taxpayer’s 2024 refund.

Then, in the smaller print, it informs the taxpayer of the reason why it is holding the taxpayer’s 2024 refund: because the taxpayer hasn’t filed their 2020-2023 tax returns and the IRS believes they will owe more tax for these years.

The IRS doesn’t want to issue the taxpayer their refund because it would prefer to assess any balance due, with penalties and interest, for the other years and then apply the taxpayer’s 2024 refund to these balances rather than issuing a cash refund to the taxpayer immediately.

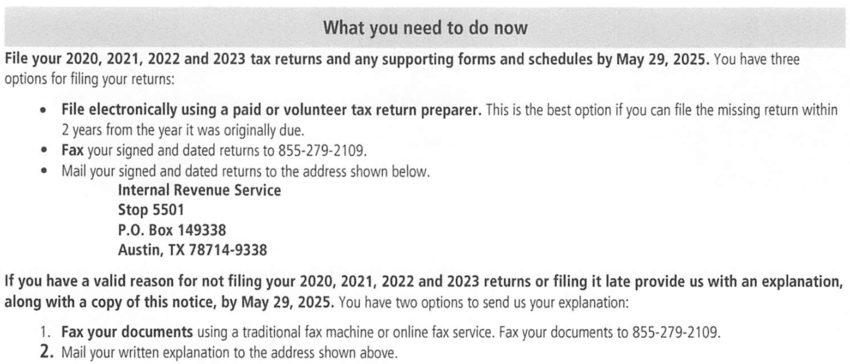

Part 2: What The IRS Needs You To Do Now

Next, the IRS will tell you what it wants you to do now — namely, file your unfiled tax returns.

The IRS provides you with three options for filing these returns:

- Filing the returns electronically using a paid or volunteer tax return preparer — obviously this option will only work for the last three years of returns since those are the only returns that can be e-filed.

- Faxing your signed and dated returns to 855-279-2109.

- Mailing your signed and dated returns to the address specified.

If you have a valid reason for not filing your tax returns or filing them late, then you should fax or mail your explanation alongside a copy of your CP63 Notice to either the fax number or the address indicated previously in the notice.

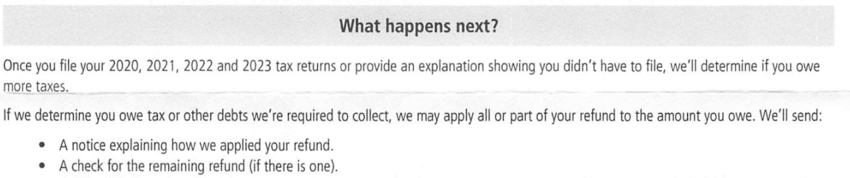

Part 3: What the IRS Says Will Happen Next

Then, the IRS will tell you what will happen after you either file your missing tax returns or provide an explanation for why you didn’t file.

After all their calculations are complete, you will receive one of two things.

They will either be:

- A notice explaining why you are not receiving your refund. This is because you owed money on your previous returns, and the refund was applied to that to cover your outstanding balance.

- A check for your remaining refund. This will be sent if there is leftover money after the IRS finishes processing your previous tax returns.

If your refund is not enough to cover your new outstanding balance, you will receive another notice with the remaining balance.

That notice will have instructions on how to pay it off, separate from your CP63 Notice.

Part 4: If The IRS Doesn’t Hear From You

Lastly, the IRS will tell you what it’ll do if they don’t hear from you within 10 days.

It will continue to hold your refund and will determine your owed taxes via a third party.

If that is the case, then your refund will continue to be held by the IRS and applied to your new outstanding balance.

Again, you will have 10 days to respond to the IRS, whether it be filing your missing tax returns or providing explanations.

Free Consultation

Behind on filing your tax returns? Let’s get you caught up.

Talk to a tax expert — free, no obligation. We prepare years of unfiled tax returns and have resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhat You Should Do If You Receive a CP63

Below are steps for you to take after you receive a CP63 Notice from the IRS.

Step 1: Confirm You Actually Need To File Your Returns

The obvious first step is to make sure you actually need to file your returns.

The IRS makes mistakes, and it’s possible that it didn’t process your returns.

Obviously, you want to get your refund as soon as possible, so check and double-check that you actually haven’t filed returns for the periods the IRS is claiming.

The best advice we can give you is to check your returns and notices to make sure you’re protecting yourself and your account.

Step 2: Dispute the Notice if the IRS is Wrong

If you believe that the IRS made a mistake, then provide an explanation as soon as possible.

You will have 10 days to take action, and this includes disputing the notice.

The IRS provided both a fax number and mailing address, but you should also be able to call them.

If you choose to contact them via fax number or mailing address, make sure you sign and date the documents.

It should also be accompanied by a copy of your CP63.

While it won’t be an easy process, it’s worth it to make sure you don’t have any holds against your account or refunds.

We provide this service to our clients, especially since we know how difficult it can be.

Often, it will take multiple phone calls and back-and-forth conversations since it’s unlikely it will be resolved right away.

Step 3: File Your Missing Returns

You will have about 10 days from the date of the notice to file your missing returns.

We advise you to file as soon as possible, lest the IRS file via a third party and charge you for the service.

You can do so electronically or in person through a tax preparer, as long as it is completed accurately and efficiently.

Doing so as soon as possible will also stop any other late filing penalties you may incur.

If this sounds overwhelming, don’t worry — we have an article on how to file back tax returns, and you can also watch the in-depth video below.

Alternative: Provide An Explanation

If you need to provide the IRS with an explanation for why you haven’t filed your tax returns, then you will still have to operate within the 10-day deadline.

There are only two acceptable methods of providing an explanation to the IRS.

- Mailing your notice.

- Faxing your notice.

You can provide an explanation (signed and dated) alongside a copy of your CP63 Notice to the IRS by mailing it to the provided address or faxing it to the provided number.

Make sure you specify which tax periods you’re providing an explanation for — that needs to be written and abundantly clear.

“Working with Luke at Choice Tax Relief has been a fantastic experience. His commitment to clear communication is what truly sets him apart. I was always impressed by his responsiveness to my questions, and his consistent, proactive updates.”

Get Help Now

Behind on filing your tax returns? Let’s get you caught up.

Talk to a tax expert — free, no obligation. We prepare years of unfiled tax returns and have resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.