IRS Form 9297: What To Do If You Received This From a Revenue Officer

IRS Form 9297, also known as the “Summary of Taxpayer Contact”, is the form that an IRS revenue officer sends to a taxpayer to inform them of:

- The documents and other information the revenue officer would like to see, along with deadlines for each, in order to determine the appropriate resolution of the taxpayer’s situation

- The consequences that the revenue officer may impose on the taxpayer if they fail to provide the requested documents and other information by the provided deadlines

- The revenue officer’s name, employee ID number, telephone number, fax number, and office address

If you’ve received Form 9297 from a revenue officer, you should not take it lightly.

The receipt of Form 9297 means that the IRS has assigned a revenue officer to your case.

This is one single, experienced collections official at the IRS whose assigned task it is to collect money from you.

The vast majority of Americans who owe the IRS do not have a dedicated revenue officer assigned to their account; their accounts are being handled by the IRS Automated Collection System (ACS), which is manned by thousands of IRS telephone employees.

There is no one IRS official in charge of your account while it’s in ACS; all collection notices you receive are automated while in ACS; but once a revenue officer is assigned to your account — beware!

There is someone at the IRS whose mission it is to get as much money from you as quickly as they can.

Table of Contents

IRS Form 9297 At a Glance

| Form Name: | Summary of Taxpayer Contact |

| Correspondence Type: | Information Request |

| Generated By: | IRS Revenue Officer |

| Preceded By: | Revenue Officer Assignment |

| Followed By: | N/A |

| Recommended Action: | Comply With Revenue Officer's Requests |

IRS Form 9297 Explained, Part by Part

Here is a full explanation of the Form 9297, part by part.

Part 1: Taxpayer and Representative Information

At the very top of the Form 9297, you’ll see some basic information:

- Taxpayer’s name: This should be your name or the name of the entity (such as a business) that you own.

- Taxpayer’s ID: This should be your Social Security number or, if the Form 9297 was issued to your business, your business’ employer identification number.

- Representative name: If you have appointed someone to be your representative on Form 2848 (Power of Attorney), their name will appear here.

This section of the Form 9297 is fairly basic, but the IRS is known to make mistakes, so be sure to review this section for accuracy and inform your assigned revenue officer of any errors.

Part 2: Standard Information and Documents Request

In the next part of the Form 9297, the revenue officer lists out some standard information and documents that he or she wants to see, along with your deadline to provide them to the revenue officer.

For a standard collections case, it’s typical for the revenue officer to request:

- The last two paystubs

- The last three months’ of bank statements

- A listing of all assets owned, such as real estate, vehicles, investments, and cryptocurrency

Finally, if you have any overdue tax returns, the revenue officer will request those as well.

You can see in the image above that this was the case for our client since the revenue officer requested delinquent 1040s for tax years 2017-2021.

The first thing we do when we are engaged by a client who has a revenue officer assigned is to call that revenue officer and request an extended deadline for the items requested.

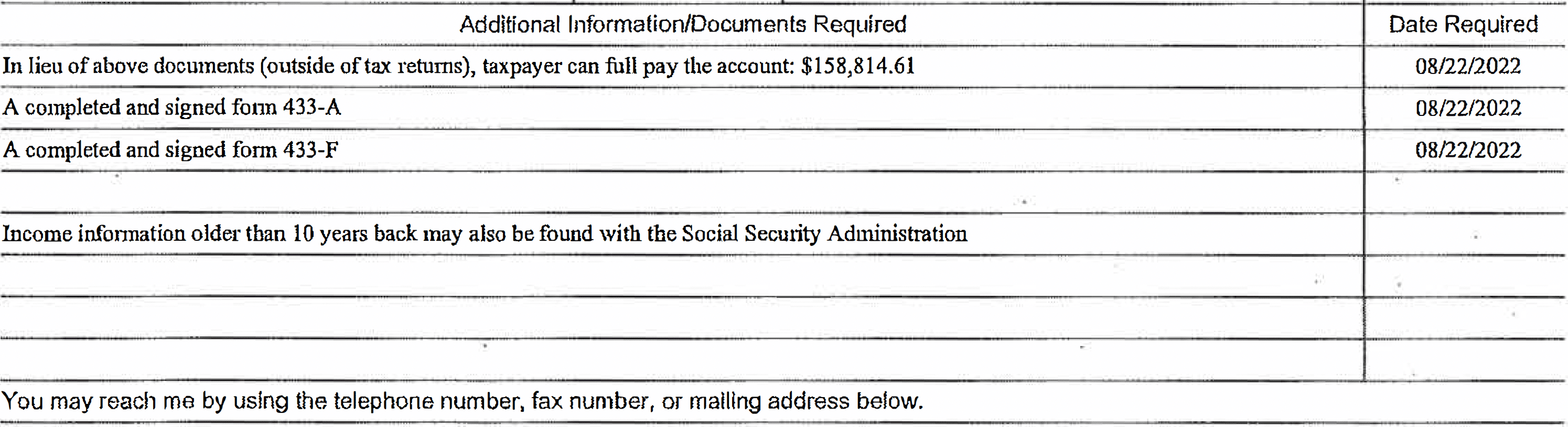

Part 3: Additional Information and Documents Request

In the next section, the revenue officer may list out additional information or documents that he or she wants to review.

It’s not uncommon for the revenue officer to request a collection information statement such as a Form 433-A so he or she can analyze your current financial situation and ability to pay your tax debt.

Part 4: Revenue Officer Contact Information

Finally, at the bottom of the Form 9297 is the revenue officer’s name and contact information.

It is in your best interest for you or your representative to make contact with your revenue officer as soon as possible!

When the IRS Sends Form 9297

The most common reason for the IRS sending you a Form 9297 is when the following things happened:

- You have a large balance due with the IRS, several years of unfiled tax returns, or both.

- The IRS assigned your case to a revenue officer.

What You Should Do If You Receive a Form 9297

Here’s what you should do, in general, when you receive a Form 9297.

Step 1: Make an electronic copy of your Form 9297.

The Form 9297 is a very important document — it tells you what information your revenue officer wants from you and by when.

So the first thing you should do is make an electronic copy of the form just in case you lose or misplace the hard copy.

Step 2: Call the revenue officer.

At a minimum, here are some things that you should request on your call:

- Any errors you spotted on the Form 9297

- Any clarification you need regarding what the revenue officer is requesting

- A request for an extension of the revenue officer’s deadlines for the information he or she requested

- Your revenue officer’s manager’s name, employee ID number, telephone number, and fax number

Step 3: Develop a game plan.

Now, step three is not simply, “Give the revenue officer everything he requested by his (hopefully extended) deadline.”

Of course, you may very well do that eventually, but before doing so you need to remember that the revenue officer is not operating in your best interest; the revenue officer is operating in the best interest of his or her employer, namely, the Internal Revenue Service, which wants to collect as much money from you as it can as quickly as it can.

So the last thing you want to do is let your revenue officer come up with a plan that’s in the IRS’ best interest; rather, you want to come up with a plan that’s in your best interest.

This could be an offer compromise; it could be getting into currently not collectible (CNC) status (also known as the IRS hardship program); it could be entering into an installment agreement with the IRS but not the one the revenue officer wants to push on you — you may want to go for a hardship-based installment agreement called a partial-payment installment agreement in which you don’t have to pay the IRS everything you owe in your installment agreement.

To learn more about these different kinds of tax relief options — “game plans” if you will — and how to come up with a game plan for your tax debt, read this article about how to get IRS tax debt relief or watch my video below.

Step 4 (If Necessary): File any overdue tax returns that are in your best interest to file.

So IRS revenue officers’ mission is two-fold: they exist to 1) collect delinquent taxes and 2) secure past-due tax returns from taxpayers.

This means that if you have unfiled tax returns, the revenue officer likely indicated on your Form 9297 that you need to provide him or her with these returns.

File the Returns as Usual

So at a minimum, you should prepare these returns — ideally have a professional prepare them to ensure you’re not reporting too much tax liability on your returns — and file them.

Give the Revenue Officer Courtesy Copies

I’ve learned from experience that you should not just hand over these returns to the revenue officer and assume that he will see to it that they’re filed; you should file these past-due returns as you normally would if there wasn’t a revenue officer involved and then give your revenue officer courtesy copies.

When I was new at representing taxpayers before revenue officers, I made the mistake one time of simply giving the tax returns the revenue officer requested from my client to the revenue officer and assuming that he would see to it that they get processed.

That did not happen; the revenue officer completely dropped the ball; ultimately the issue was resolved; but it caused a lot of unnecessary confusion and caused the case to drag on because I trusted the revenue officer to file the returns.

So ever since then, my policy is to file clients’ returns as I normally would if there were no revenue officer involved and then simply give the revenue officer a courtesy copy.

You May Want to File Returns Beyond What Was Requested

Now, one last word about unfiled tax returns before we move on.

On the Form 9297, the revenue officer is likely only requesting that you provide him or her with the tax returns that are necessary to get you in “compliance” with the IRS for purposes of resolving your tax debt.

And that’s generally limited to the last six years of tax returns.

However, the IRS may have filed a substitute for returns (SFRs) for other tax years, in which case it may be in your best interest to file those years as well.

By way of example, the client whose Form 9297 I’m using as a (sanitized) example in this article did not file many years of tax returns in the late 2000s and early 2010s, and the IRS actually prepared SFRs for him for tax years 2007 and 2011.

And actually the $158,814.61 balance on the Form 9297 was entirely attributed to these SFRs.

And guess what?

The revenue officer didn’t request returns for these years because in his mind the returns were already done; the IRS had prepared SFRs for those years; he wasn’t going to volunteer that it would likely be in the taxpayer’s best interest to file original returns for those years.

But this taxpayer was 1099, meaning that he was entitled to take deductions against his income for these years — deductions the IRS didn’t include in their SFRs because the IRS would have no way of knowing what those deductions were.

Additionally, this taxpayer was abroad for one of these years the IRS prepared an SFR for, meaning that he qualified for the foreign earned income exclusion for that year, which on top of his business deductions, significantly reduced his tax liability for that year.

And simply by filing these returns — that the revenue officer did not ask for, mind you — we were able to reduce this client’s liability by over $90,000.

And this goes back to the previous step of developing your own game plan and not just being a little yes-man or yes-woman to your revenue officer because you’re scared of him or her and letting him or her call the shots; you need to advocate for yourself and if you’re not comfortable doing that you need to hire someone who will advocate for and represent you before the revenue officer.

Not sure where to start when preparing back tax returns? Read this article or check out my video below!

Step 5: Provide the requested information to the revenue officer along with your game plan.

So yes, you will eventually provide the requested information to the revenue officer.

But you will also communicate to him or her your game plan for how to address your tax issue.

And here’s where the fun begins because your revenue officer likely has a very different game plan for how to resolve your tax issue than you do.

And that leads me to step six.

Step 6: Know your rights and fight tooth and nail.

Revenue officers are, in general, not rookie IRS collections employees.

Many of them have advanced degrees in taxation, and some of them are attorneys.

Many of them have been with the IRS for decades.

So you should be very prepared for revenue officer to disallow many of your necessary living expenses that you’re indicating on you Form 433-A.

I don’t want to get too into the weeds here, but essentially your revenue officer is going to try to position you as well-off as possible, spending your money on unnecessary expenses, because if you’re well off then you can afford to pay the IRS back everything you owe.

On the other hand, it’s usually the case where we try to position our clients as broke as possible with the only things they’re spending money on being basic living expenses that are necessary for the health and welfare of themselves and their family or for the production of income, meaning that they’re not going to be able to afford to pay the IRS right now what they owe in full and maybe ever.

So while the revenue officer may be pushing for a full-payment installment agreement, we might be pushing for a partial-payment installment agreement because we believe we can show, by the IRS’s own policies as set forth in the Internal Revenue Manual for how to determine how much money a taxpayer has to pay toward their tax debt IRS, that the taxpayer really only can afford to pay the IRS fifty dollars a month or something like that (depending on the situation).

It’s not always that extreme or that low a figure, but that’s the gist of the fight here between you or your representative and your revenue officer.

If you want to learn more about how to fight the IRS, read this article or check out my video below!

“A special thank-you to Nathan and Luke for their help and professionalism throughout the entire process. They assisted me in getting four tax years filed, working directly with the necessary entities on my behalf.”

Free Consultation

Owe the IRS? Don’t wait for their next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXGet Help Now

Owe the IRS? Don’t wait for their next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.