IRS Letter 1058: What It Is, What It Means, and How to Respond

IRS Letter 1058 is the Final Notice of Intent to Levy and Your Right to a Collection Due Process Hearing that a revenue officer sends to a taxpayer before he or she intends to start seizing the taxpayer’s income and property in order to satisfy the taxpayer’s debt to the IRS.

The IRS revenue officer will send Letter 1058 via certified mail.

Here is a redacted Letter 1058 that an IRS revenue officer sent one of our clients.

Table of Contents

IRS Letter 1058 At a Glance

| Notice Type: | Collections |

| Generated By: | IRS Revenue Officer |

| Preceded By: | CP504 |

| Followed By: | Levy Action |

| Accompanied By: | Form 12153 |

| Recommended Action: | Negotiate With Revenue Officer |

IRS Letter 1058 Explained, Part by Part

Here is a full explanation of the Letter 1058, part by part.

Note that the Letter 1058 is often accompanied by the Form 12153 that you use to request a collection due process hearing.

Part 1: Notice of Intent to Levy and Your Right to a Collection Due Process Hearing

At the top of the Letter 1058, you’ll see the name of the letter, which also informs you of the two purposes that it serves:

- To inform you that the IRS intends to levy — that is, seize — your assets and income streams in order to satisfy your tax debt.

- To give you notice that you have the right to request a collection due process (CDP) hearing to propose an alternative to the IRS levying you.

Part 2: Why the IRS Is Sending You This Letter

Next, IRS Letter 1058 informs you of why the IRS is sending this letter, namely, because the IRS has asked you to pay your unpaid tax liability but it still hasn’t received your payment.

Therefore, the IRS now intends to levy you — that is, to take your things in order to satisfy your back taxes.

However, before the IRS can do this, it must give you notice of the following two things, which it accomplishes in this letter:

- Notice of the IRS’s intent to levy you: Internal Revenue Code Section 6331(d)(2) requires that, no less than 30 days before the levy action occurs, the IRS notifies the taxpayer of their intent to levy the taxpayer as well as the basic rules concerning IRS levies.

- Notice of your right to a collection due process (CDP) hearing: Internal Revenue Code Section 6330 requires that, no less than 30 days before the levy action occurs, the IRS notifies the taxpayer of their right to a CDP hearing.

This part of the IRS Letter 1058 informs you of these things.

Part 3: What the IRS Says You Need to Do

Next, the IRS tells you what you “need” to do — and, as expected, they want you to “pay in full today.”

The reality, however, is that if you can’t afford to pay in full today — and even if you can — you have options.

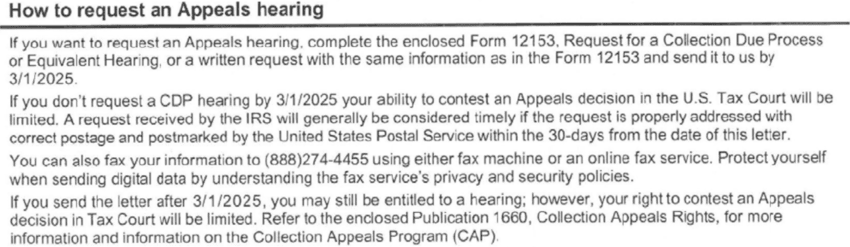

Part 4: How to Request an Appeals Hearing

This is probably the most important section of your Letter 1058.

In this section, the IRS gives you (brief) instructions about how to appeal the IRS’s levy action.

To do this, you must complete the Form 12153, Request for a collection due process or equivalent hearing.

You must submit this form to the IRS no later than 30 days after the date of your Letter 1058.

If you fail to do so, you may still submit the Form 12153 — but you will not get a collection due process (CDP) hearing; you will get an equivalent hearing.

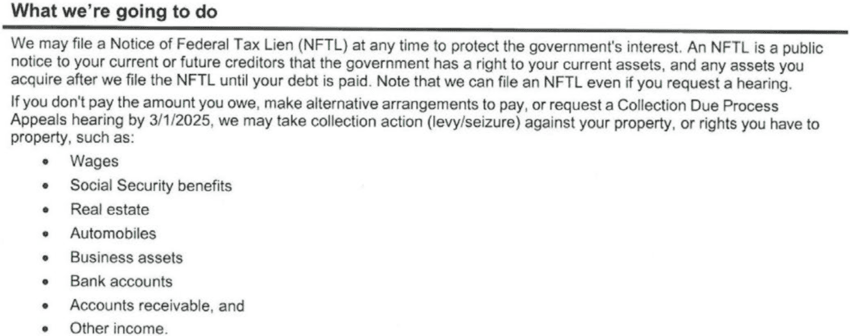

Part 5: What the IRS Says They’re Going to Do

Next, the IRS tells you what they’re going to do if you don’t pay what you owe them.

These actions include:

- Filing a Notice of Federal Tax Lien (NFTL)

- Seizing (i.e., levying) your property or rights to property unless you make some arrangement with your revenue officer or request a CDP hearing to plead your case before an appeals officer

Although some property is exempt from levy, the IRS can seize the majority of your property and income sources, including:

- Wages

- Social Security benefits

- Real estate

- Automobiles

- Business assets

- Bank accounts

- Accounts receivable

- Other income

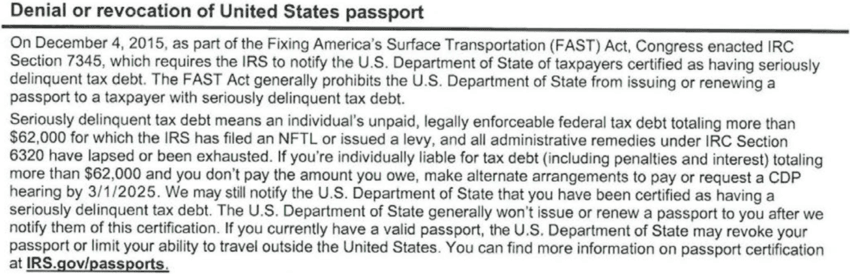

Part 6: Denial or Revocation of United States Passport

If you owe enough in back taxes — the threshold is currently $62,000 — the IRS may prevent you from obtaining or renewing your passport.

It does this by “certifying” your tax debt to the United States Department of State — basically, telling the State Department that you owe a lot in taxes and therefore it should deny any passport applications you submit.

In certain cases, the State Department may even revoke your existing passport.

So if you are outside the United States — or are planning to travel outside the United States in the near future — it’s essential that you deal with your federal tax debt!

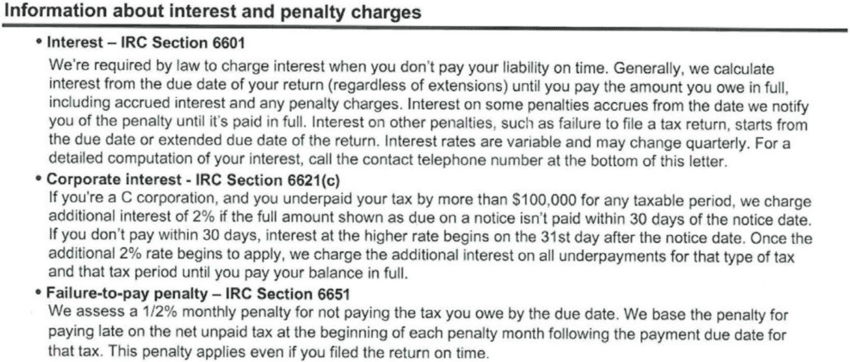

Part 7: Information About Interest and Penalty Charges

Next, the IRS provides you some information about interest and penalty charges it may charge you.

Interest Under Internal Revenue Code Section 6601

The tax code requires the IRS to charge taxpayers interest on their unpaid taxes.

Interest starts accruing on the date your taxes are due and compounds daily not only on your underlying tax liability but also on penalties and the interest itself.

For more information about how the IRS calculates interest, read this article or watch the video below.

Corporate Interest Under Internal Revenue Code Section 6621(c)

Corporate taxpayers who owe more than $100,000 for any taxable period are liable for an additional 2% interest charge on their balance.

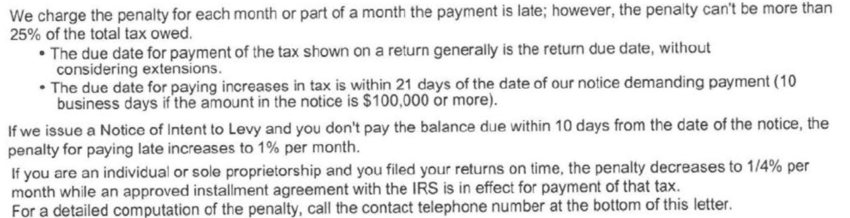

Failure-to-Pay Penalty Under Internal Revenue Code Section 6651

If you don’t pay your tax by its due date, the IRS will charge you a failure-to-pay penalty in addition to the interest described above.

This penalty is generally equal to 0.5% of your tax liability for every month or part of a month it goes unpaid, up to a maximum of 25%.

Here are some circumstances in which the failure-to-pay penalty may differ from the standard 0.5% per month:

- An increase to 1% per month if the taxpayer has been issued a notice of intent to levy and the taxpayer does not pay the balance due within 10 days from the date of the notice

- A decrease to 0.25% per month if the taxpayer is in an approved installment agreement with the IRS for the tax and the taxpayer timely filed their tax return for the tax

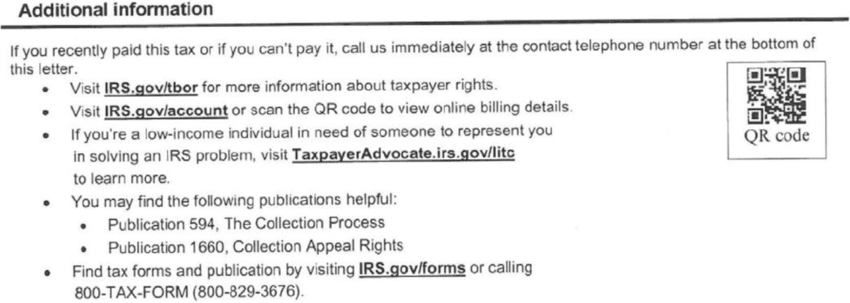

Part 8: Additional Information

Next, the IRS provides some additional information, such as:

- The official IRS webpage for the Taxpayer Bill of Rights

- The IRS webpage where you can create an IRS online account

- The Taxpayer Advocate’s webpage about low-income taxpayer clinics (LITC)

- A list of two publications that you may find helpful:

- Where to obtain tax forms, instructions, and publications

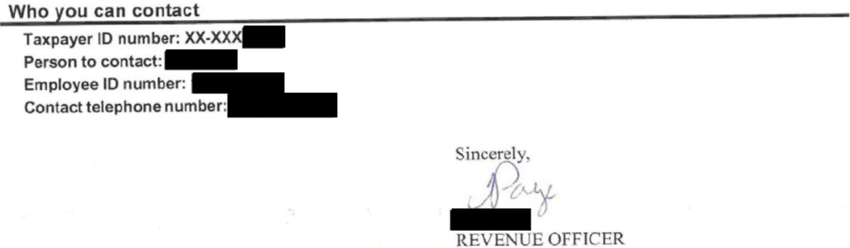

Part 9: Revenue Officer Contact Information and Signature

Next, the IRS provides you with the contact information, including employee identification number and telephone number, for the IRS revenue officer handling your case.

Part 10: Enclosures

Next, the IRS tells you of the enclosures — that is, the other documents — it has enclosed in the same envelope as your Letter 1058.

Typically, this includes:

- A copy of the Letter 1058

- Publication 594

- Publication 1660

- Form 12153

Part 11: Table of Amount You Owe

Finally, the IRS provides you with a table of the amount you owe by period, including penalties, interest, and total.

When the IRS Sends Letter 1058

The IRS typically sends the Letter 1058 to a taxpayer when:

- A revenue officer has been assigned to their account.

- The taxpayer owes money to the IRS — or at least the IRS believes the taxpayer owes money to the IRS.

- The IRS has sent other collections notices to the taxpayer — typically, at the very least, a CP14 Notice and a CP504 Notice (or their equivalents).

- The taxpayer has not paid off this tax debt or entered into some kind of resolution with the IRS for it.

What You Should Do If You Receive a 1058 Letter

Below are the steps you should take after you receive a Letter 1058.

For more information about each of these steps, check out our article How to Fight the IRS and Win.

Step 1: Check the Letter 1058 for accuracy.

Don’t assume that the IRS did their math correctly — review the IRS’s numbers against your own.

Step 2: Correct any errors with the IRS.

If you do find an error in the IRS’s math, take it up with your revenue officer.

You can always reach out to us at at 866-8000-TAX to go to bat against the IRS for you.

Step 3: Seek Penalty Abatement.

For most of our clients with penalties on their account, we at least seek some sort of penalty relief for them.

Sometimes the IRS grants it; sometimes they don’t.

But it’s generally at least worth a shot.

For more information about seeking abatement for the penalties on your account, check out this article.

Step 4: Consider requesting a CDP hearing.

It may be in your best interest to request a CDP hearing to protest the IRS’s proposed levy action.

Of course, if you do this, you should have some workable collection alternative in mind to propose as an alternative to levy action, such as gathering funds to pay off the balance due or seeking some tax relief alternative (see below).

Step 5: Pay the Balance Due OR Seek Tax Relief

Finally, you have to figure out what to do with the amount you owe the IRS after you’ve cleared up any disagreements with them concerning the amount as well as obtained any possible penalty relief for your account.

You can, of course, pay off your balance in full. This will (obviously) stop future penalties and interest from accruing.

However, a better option — if you qualify for it — is an offer in compromise. An offer in compromise is an agreement you make with the IRS in which the IRS agrees to accept a lower amount to satisfy your tax debt than you actually owe.

That said, not all taxpayers qualify for an offer in compromise, so there are other options, such as a temporary hardship placement called currently not collectible status as well as installment agreements for taxpayers who wish to pay their balance over time.

For an overview of how tax relief works, read our article What Is Tax Relief and How Does It Work?.

IRS Letter 1058 vs. IRS Letter 1058-A

IRS Letter 1058 is very similar to IRS Letter 1058-A in that they are both the final notice an IRS revenue officer will send a taxpayer before they intend to levy them.

The main difference is in the type of debt — joint or single — the taxpayer owes.

If the taxpayer owes joint tax debt, they will receive a Letter 1058-A; if they owe single tax debt, they (along with whomever they share the joint tax debt with) will receive Letter 1058 (without the “-A”).

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.