IRS Notice CP14: What It Is and How to Respond

The IRS Notice CP14 is usually the first bill you receive when you file a return showing a balance due (or the IRS calculates that you owe more than you paid).

Officially a Notice of Tax Due and Demand for Payment, it tells you exactly how much you owe — tax, penalties, and interest — and gives you a date by which to pay.

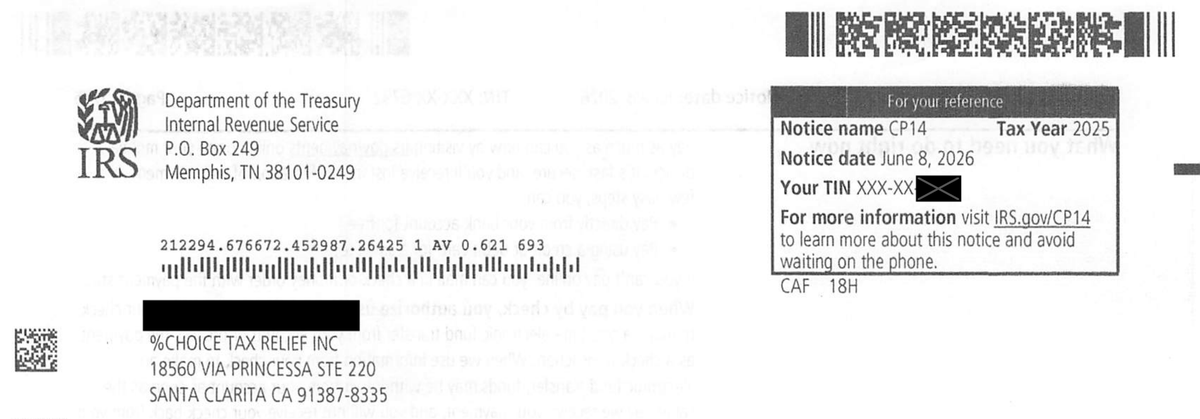

Here is a redacted CP14 Notice that one of our clients received.

Below, we walk through the current version of the CP14 line by line, explain how the IRS built your balance, and lay out your options — whether you can pay in full, need time to pay, or want to challenge the amount.

Key Takeaways

- IRS Notice CP14 is the IRS’s first balance-due notice — it shows the tax you reported, plus penalties and interest, and demands payment by a set date (June 29, 2026 on this client’s notice).

- Your total is broken into three pieces: tax ($38,005.00 on this client’s notice), penalties ($1,526.38), and interest ($338.83), for an amount due of $39,870.21.

- If you already have an installment agreement for this tax year, keep paying it — the CP14 does not cancel it.

- If you can’t pay in full, you have options: a payment plan, an offer in compromise, or a temporary collection hold. Penalties and interest keep growing until the balance is paid.

- Ignoring a CP14 leads to more notices (CP501, CP503, CP504) and eventually IRS collection action such as liens and levies. It is far cheaper to act now.

Table of Contents

The CP14 Series of IRS Notices

The CP14 is the IRS’s most common first “Notice of Balance Due,” and the IRS issues the same first bill in several closely related versions, each marked with a different letter after “CP14.”

The table below shows how the CP14 compares to those other versions so you can confirm exactly which notice you received and what it means.

| Notice | What It Is | When the IRS Sends It |

|---|---|---|

| CP14 | The IRS's standard first bill for unpaid taxes — the most common balance-due notice it sends. | After you file a return showing a balance due and don't pay it in full by the return's due date. |

| CP14C | A CP14 issued with a disaster-relief cover page that postpones your payment deadline. | When your address of record is in a federally declared disaster area; penalties and interest are paused until the relief period ends. |

| CP14D | The same first bill in the IRS's redesigned “scan-and-pay” layout, with a QR code and resolve-your-balance boxes. | After you file with a balance due and don't pay by the due date — same meaning as a CP14, newer format. |

| CP14E | A version of the first balance-due notice, issued under IRC § 6303 just like the CP14. | After you file with a balance due and don't pay in full — in our experience, often after filing Form 1040-SR (the return for seniors). |

| CP14F | A version of the IRS's first bill in its redesigned “Notice of Balance Due” format. | After the IRS processes your return, finds the tax you reported exceeds your payments and credits, and you haven't paid the balance. |

| CP14G | Another version of the redesigned first bill for unpaid taxes. | After the IRS processes your return, sees an amount due, and doesn't receive full payment by the return's due date. |

| CP14IA | The installment-agreement version — confirms your payment plan is set up while the balance keeps accruing penalties and interest. | After you successfully set up an installment agreement (payment plan) on a balance you owe. |

| CP14J | The failure-to-pay-penalty version — your balance is unpaid tax plus a failure-to-pay penalty and interest. | After you file on time but don't pay in full, so a failure-to-pay penalty (but no failure-to-file penalty) applies. |

| CP14K | A version of the IRS's first bill, nearly identical in meaning to the CP14. | After you file a return with an amount owed and some balance remains unpaid once your payments and credits are applied. |

IRS Notice CP14 At a Glance

| Question | Answer |

|---|---|

| What is it? | The IRS’s first bill — a Notice of Tax Due and Demand for Payment for a balance on your account. |

| Why did I get it? | You filed a return with tax owed that wasn’t fully paid, or the IRS adjusted your account to show a balance. |

| Do I need to respond? | Yes — pay by the due date, set up a payment option, or dispute the balance if it’s wrong. |

| What’s the deadline? | The pay-by date on the notice (June 29, 2026 on this client’s notice). |

| What if I ignore it? | Penalties and interest keep accruing, and the IRS escalates to CP501, CP503, and CP504 — then liens and levies. |

IRS Notice CP14 Explained, Part by Part

Here is a full explanation of the CP14, part by part, based on the IRS’s current CP14 format.

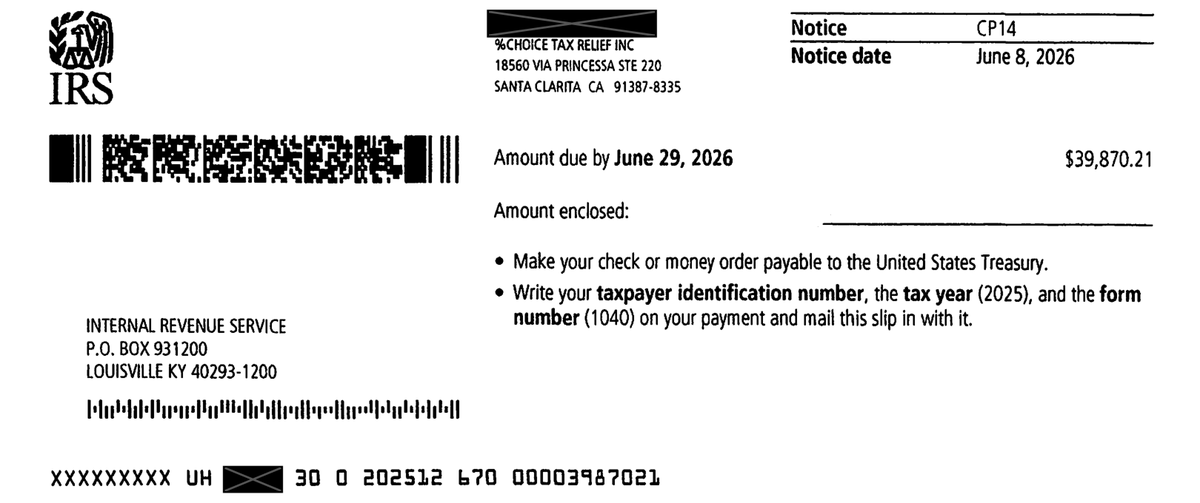

Part 1: Notice Header and Amount Due

The top of the notice identifies it as a CP14 and lists the key reference details in the box on the right:

- The tax year (2025 on this client’s notice)

- The notice date (June 8, 2026)

- Your taxpayer identification number

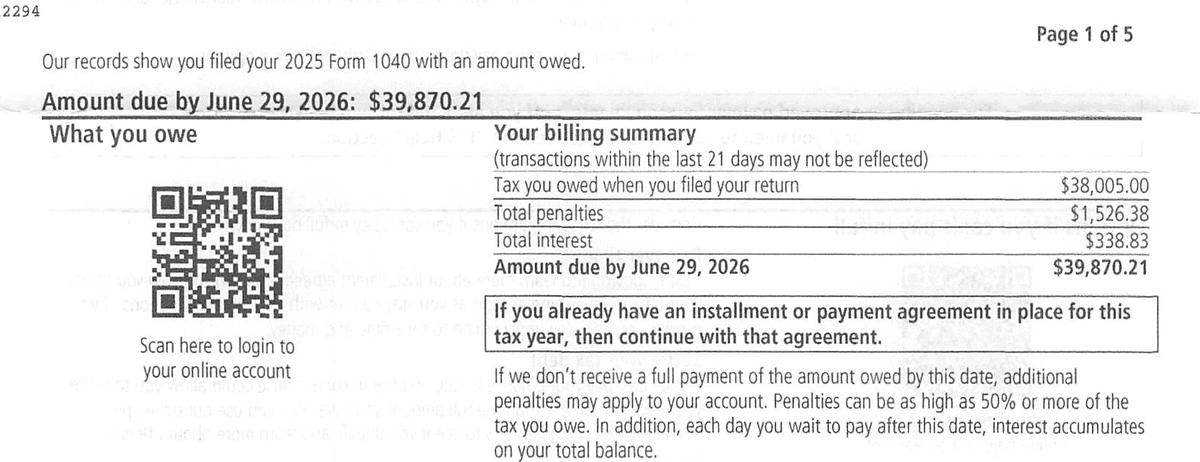

Just below, the IRS states the reason plainly — “Our records show you filed your 2025 Form 1040 with an amount owed” — and gives you the headline figure: an amount due of $39,870.21 by June 29, 2026.

Part 2: What You Owe — Your Billing Summary

The billing summary breaks your balance into three parts:

- The tax you owed when you filed — $38,005.00 on this client’s notice

- Total penalties — $1,526.38

- Total interest — $338.83

Together, these add up to the amount due of $39,870.21.

The notice also reminds you that if you already have an installment or payment agreement in place for this tax year, you should continue with it.

Note the warning: penalties can climb to 50% or more of the tax you owe, and interest is added every day you wait.

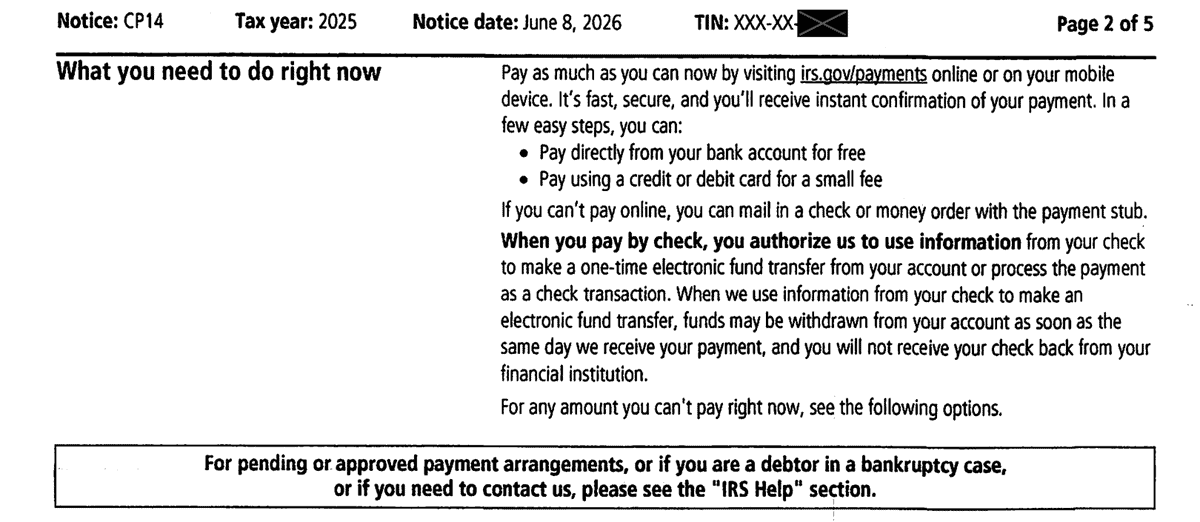

Part 3: What You Need to Do Right Now

The IRS asks you to pay as much as you can now, ideally online at irs.gov/payments — directly from a bank account for free, or by credit or debit card for a small fee.

If you can’t pay online, you can mail a check or money order with the payment stub.

The notice also includes standard check-conversion language: paying by check authorizes the IRS to process it as a one-time electronic funds transfer.

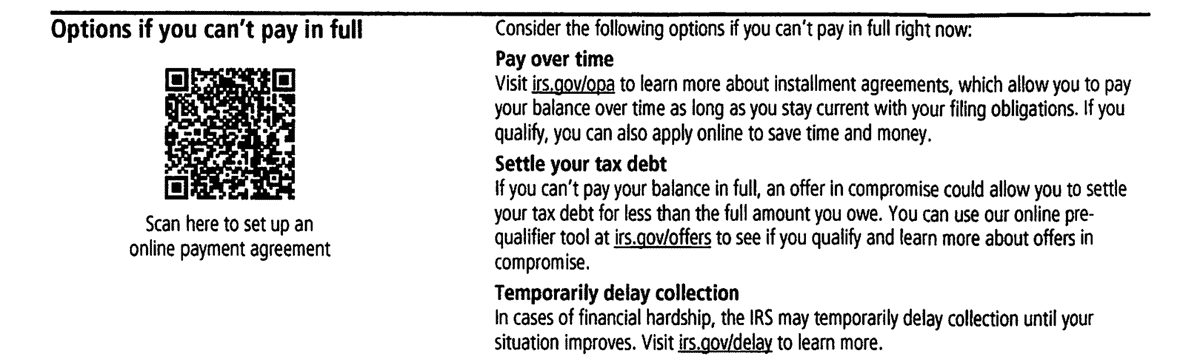

Part 4: Options If You Can’t Pay in Full

This section lays out three paths if paying in full isn’t realistic.

Pay over time with an installment agreement (irs.gov/opa) as long as you stay current on future filings.

Settle your tax debt for less than the full amount through an offer in compromise (irs.gov/offers) if you qualify.

Or, in cases of genuine financial hardship, ask the IRS to temporarily delay collection (irs.gov/delay) until your situation improves.

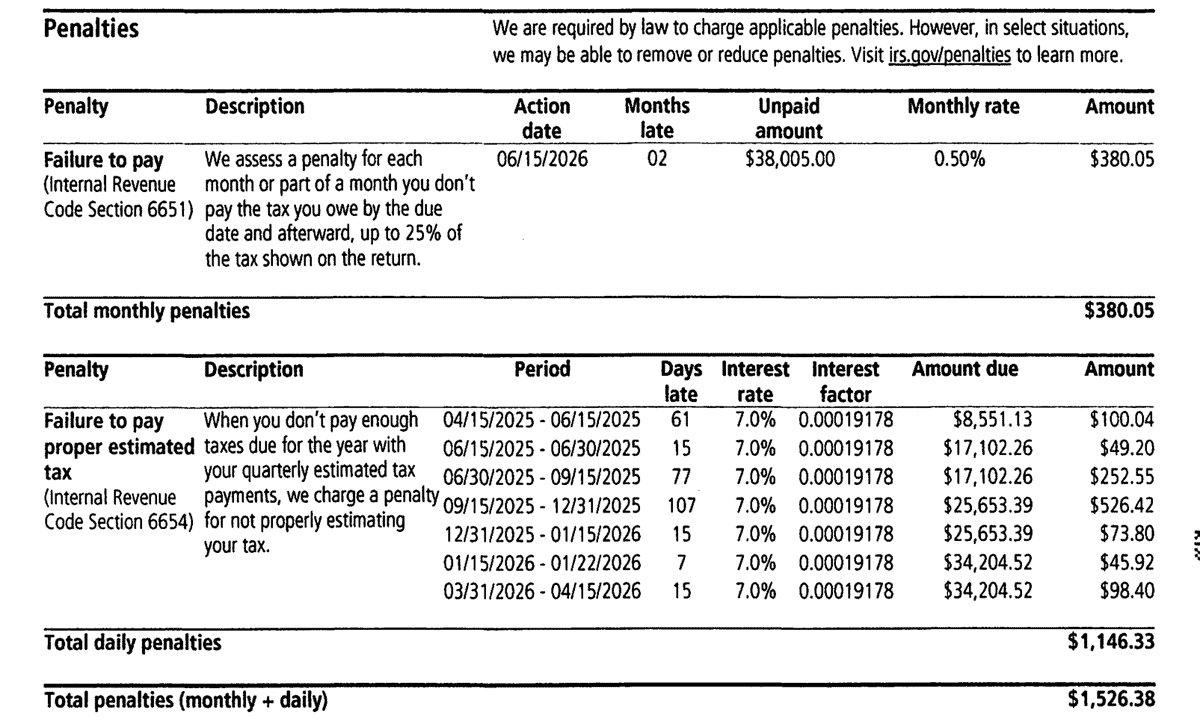

Part 5: Penalties

The penalties page shows exactly how the IRS calculated the $1,526.38.

On this client’s notice there are two:

- A failure-to-pay penalty under IRC §6651 ($380.05, assessed monthly at 0.50% of the unpaid tax)

- A failure-to-pay-proper-estimated-tax penalty under IRC §6654 ($1,146.33, calculated daily across several periods)

The IRS notes that in select situations it can remove or reduce penalties — more on that below.

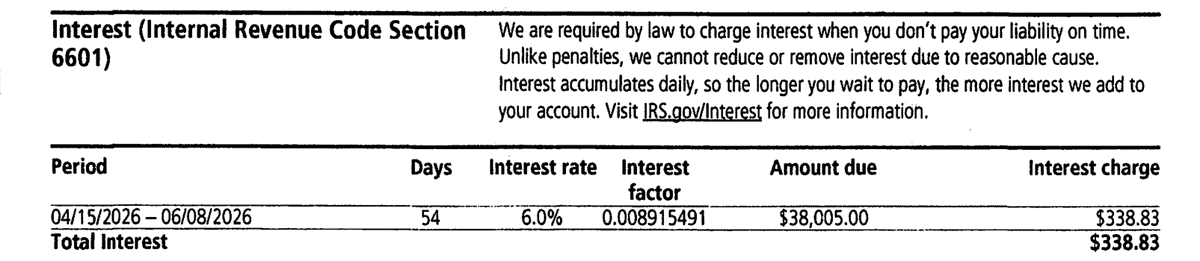

Part 6: Interest

Interest is charged under IRC §6601 and, unlike penalties, generally can’t be removed for reasonable cause.

On this client’s notice the IRS charged $338.83 at a 6.0% annual rate for the period from April 15, 2026 to the notice date.

Because interest compounds daily, the longer the balance sits unpaid, the more it grows.

Part 7: Payment Stub

The last page is a detachable payment stub to include if you mail a check.

It repeats the amount due and due date and tells you to make your check payable to the United States Treasury and to write your taxpayer identification number, the tax year (2025), and the form number (1040) on the payment.

Mail it to the address on the stub (an IRS payment center in Louisville, KY on this client’s notice).

Free Consultation

Got a CP14 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhen Does the IRS Send Notice CP14?

The IRS sends a CP14 after it processes a return that shows a balance due — or after it adjusts your account and determines you owe more than you paid — and that balance hasn’t been paid in full.

It is the opening notice in the IRS collection cycle.

In most cases you’ll receive it within a few weeks of filing a return with tax owed, and it is the first in a series of increasingly urgent notices if the balance goes unpaid.

What Should You Do If You Receive a CP14 Notice?

A CP14 is serious, but you have clear options.

Here is what we recommend.

Step 1: Verify the CP14 for Accuracy

Compare the notice to your filed return and payment records.

Check the tax, the payments the IRS credited, and the penalty and interest math.

If the balance looks wrong — a missing payment, a return the IRS changed, or a duplicate assessment — that’s something to resolve before you pay.

Step 2: Pay the Balance in Full If You Can

If the amount is correct and you can afford it, paying in full by the due date stops penalties and interest from growing.

Pay online at irs.gov/payments (free from a bank account) or mail a check with the stub.

Paying promptly is almost always the cheapest path.

Step 3: If You Can’t Pay in Full, Choose a Resolution Option

If full payment isn’t possible, set up an installment agreement (irs.gov/opa), explore an offer in compromise to settle for less than you owe, or request currently-not-collectible status if paying anything would create hardship.

Choosing an option quickly keeps your account out of enforced collection.

Step 4: Ask About Penalty Relief

If this is your first balance-due notice in a while, you may qualify for first-time penalty abatement, and if a genuine circumstance caused the late payment, you can request reasonable-cause relief.

The failure-to-pay and estimated-tax penalties on a CP14 are often reducible even when the tax and interest are not.

Step 5: Don’t Let It Escalate

Whatever you decide, act before the due date.

A CP14 that goes unanswered is followed by reminder notices and, eventually, enforced collection.

If the balance is large or you’re unsure of your best option, talk to a licensed tax professional who can deal with the IRS on your behalf.

What Happens If You Ignore a CP14?

If you don’t pay or respond, the IRS keeps adding penalties and interest and moves you through its collection notice stream:

- The CP501 reminder

- Then the CP503

- Then the CP504, which is a notice of intent to levy your state tax refund

From there the IRS can issue a final notice of intent to levy and file a federal tax lien, putting your wages, bank accounts, and property at risk.

Every step is avoidable by responding to the CP14 early.

IRS Notice CP14: Frequently Asked Questions

What is IRS Notice CP14?

IRS Notice CP14 is the IRS’s first bill — an official Notice of Tax Due and Demand for Payment. It shows the tax you owe plus penalties and interest and asks you to pay the balance by a date printed on the notice.

Why did I get a CP14 if I already filed my return?

A CP14 goes out when you filed a return showing tax due that wasn’t fully paid, or when the IRS adjusted your account and found a balance. It can also arrive if a payment you made hasn’t posted yet — always compare it against your own records before paying.

What should I do if I can’t pay my CP14 in full?

You have options: set up an installment agreement at irs.gov/opa, apply for an offer in compromise to settle for less than you owe, or request currently-not-collectible status if paying would cause hardship. Choosing one quickly keeps your account out of enforced collection while penalties and interest continue to accrue.

Can the penalties on a CP14 be removed?

Often, yes. The failure-to-pay and estimated-tax penalties on a CP14 may qualify for first-time penalty abatement or reasonable-cause relief. Interest, by contrast, generally cannot be removed unless it was charged in error.

What happens if I ignore a CP14 notice?

Penalties and interest keep growing and the IRS escalates through its collection notices — CP501, CP503, and CP504 — and can then file a federal tax lien and levy your wages, bank accounts, or other property. Responding to the CP14 early avoids all of that.

How do I pay a CP14?

The fastest way is online at irs.gov/payments — free directly from a bank account, or by card for a small fee. You can also mail a check or money order made payable to the United States Treasury with the payment stub, writing your taxpayer identification number, the tax year, and Form 1040 on it.

“Their team of experts saved me a staggering $23,000 in taxes owed to the IRS. From the initial consultation to the final resolution, they demonstrated exceptional professionalism, knowledge, and dedication.”

Get Help Now

Got a CP14 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.