IRS Notice CP161: What To Do When You Have An Outstanding Balance

IRS Notice CP161 is typically the first notice the IRS sends to your business after it files a tax return showing an unpaid balance due.

It will inform you about your outstanding balance, along with any penalties and interest you may have incurred due to non-payment.

If not responded to, the CP161 is typically followed by the CP504B.

The CP161 is one of the notices that meet the standards described in Internal Revenue Code § 6303, which requires the IRS — within 60 days of assessing a tax — to send taxpayers a notice of how much tax they owe and demand that they pay it.

For businesses, the CP161 is the most common notice that the IRS sends to satisfy the § 6303 requirement; for individuals, the corresponding notice is the CP14.

If the IRS levies your business without sending you the CP161 or an equivalent notice and demand, the levy is improper and you should contest it.

The CP161 is an example of a type of notice the IRS must send before levying you.

Note, of course, that the IRS may be sending you notices at an old address!

Here is a redacted Notice CP161 that the IRS sent to one of our clients.

Table of Contents

IRS Notice CP161 At a Glance

Notice Type: Notice and Demand Generated By: IRS Service Center Preceded By: Typically, Filing of a Tax Return Showing a Balance Due Followed By: CP504B Recommended Action: Pay Off Balance or Enter Into Resolution

IRS Notice CP161 Explained, Part by Part

Here is a full explanation of the Notice CP161, part by part.

Part 1: Balance Due

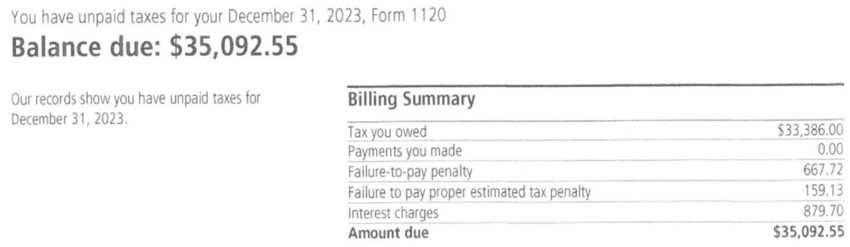

First, the IRS will provide you with a billing summary for the tax period to which the CP161 pertains

The outstanding balance will be at the top, along with its time period.

Each notice is specific to the time period the balance is for, so it’s possible to receive more than one if you owe for multiple tax periods.

Then, you’ll be provided with a breakdown of the balance.

The tax balance will be at the top, followed by the payments, which would reduce the balance, and other penalties.

Of course, the billing summary will also provide you with the interest charges that accrue starting from the date the balance was incurred as well as your total amount due.

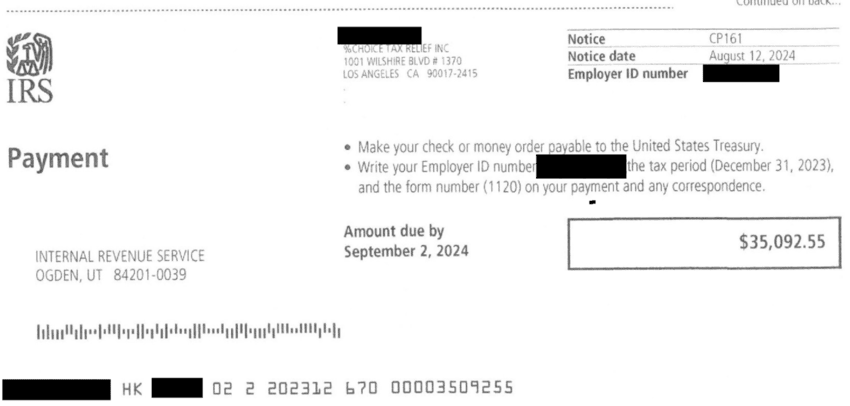

Part 2: Payment Coupon

Next, you’ll be provided with a payment coupon.

Obviously, the IRS wants you to pay them in full.

If you have the means to do so, then you could use the payment coupon it provides.

The coupon will allow you to pay your balance in full via check or money order.

You’ll mail it to the address on the coupon or the one at the top of the letter.

Don’t forget to write your business’ EIN, the tax period, and the form number on your payment so the IRS knows what you’re paying for.

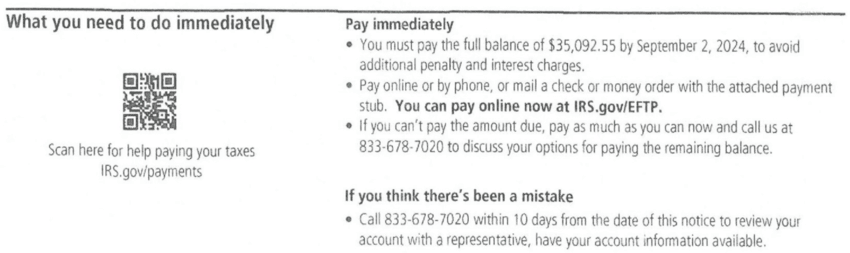

Part 3: What the IRS Says You Need to Do Immediately

Then, the IRS will tell you what you need to do immediately.

Obviously, like we said before, the IRS will want you to pay them immediately.

Again, you can pay via the payment coupon or online at their website.

If you cannot pay, they provide a phone number to discuss your options for payment.

Sometimes the IRS makes mistakes, and you shouldn’t be afraid to call them out on them.

If you find a mistake (or even what looks to be a mistake), then call them within ten days of the date of the notice.

They will review your account with a representative to double-check.

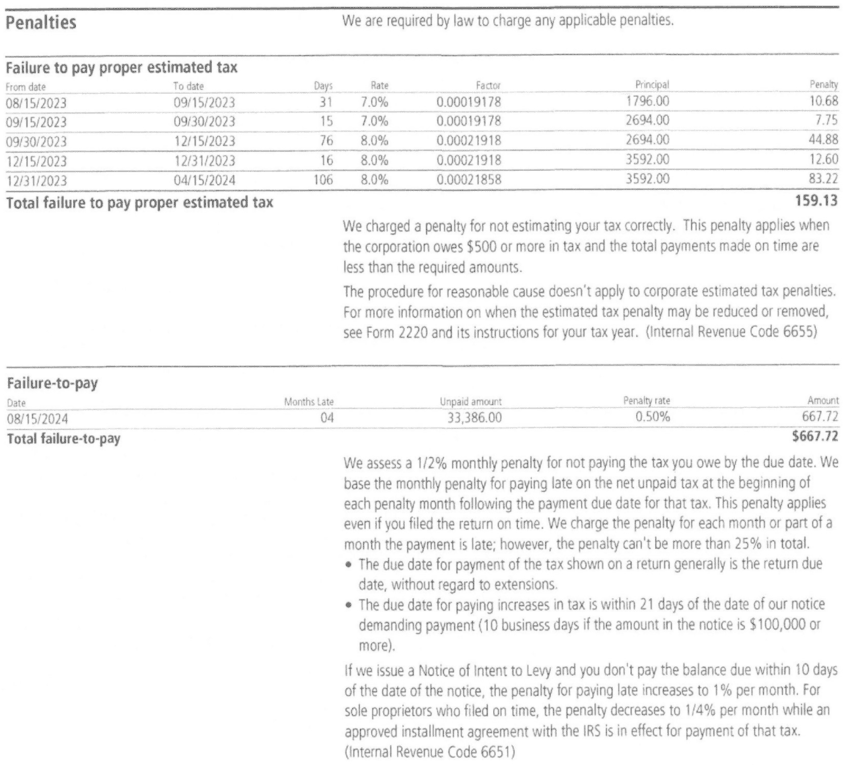

Part 4: Penalties Breakdown

Then, the IRS will provide you and your business with a breakdown of your penalties on your outstanding balance.

Possibly penalties include:

- The failure-to-pay-proper-estimated-tax penalty: This penalty is imposed on a corporation when it owes $500 or more for the tax year and did not make timely estimated tax payments during the year.

- The failure-to-pay penalty: This is a 0.5% monthly penalty for not paying your balance. If there is no payment, but an intent to levy is issued, the percentage increases to 1%. On the flip side, sole proprietors filing on time can see their penalty decrease to 0.25%. This penalty is capped at 25% of the balance due.

- The failure-to-file penalty: Although our client above was not charged this penalty, it is equal to a penalty of 5% of the balance due per month that the business return was filed late. This penalty is capped at 25% of the balance due.

If you cannot pay all the penalties your balance is incurring, the IRS provides some options for balance relief.

If you contact them for specific penalties with written explanations for reconsideration of the fees, the IRS will take some action.

However, the requests require documentation and signed statements for each request being made.

Lastly, if you were penalized after following the IRS’s written advice, penalties may be removed on the basis of the erroneous IRS advice.

Here are the four examples the IRS provides that qualify an individual for penalty removal.

- You wrote to the IRS asking for written advice on a specific issue.

- You gave the IRS adequate and accurate information.

- You received written advice from the IRS.

- You reasonably relied on the IRS’s written advice and were penalized based on that advice.

If one or more of these are true, then you can qualify for the removal of your penalties.

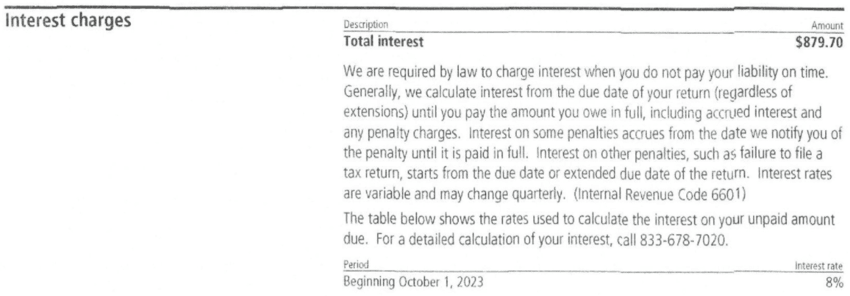

Part 5: Interest Charges

Next, the IRS will provide you with your total interest charges.

They are required by law to charge you, generally charging monthly from the date of the return.

It will also give you the interest rate it uses and the time period it started charging you.

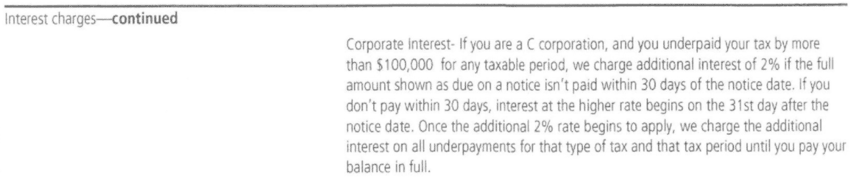

If your business happens to be a C-corporation that underpaid by $100,000 or more, there will be an additional 2% interest charge if payment isn’t received within 30 days.

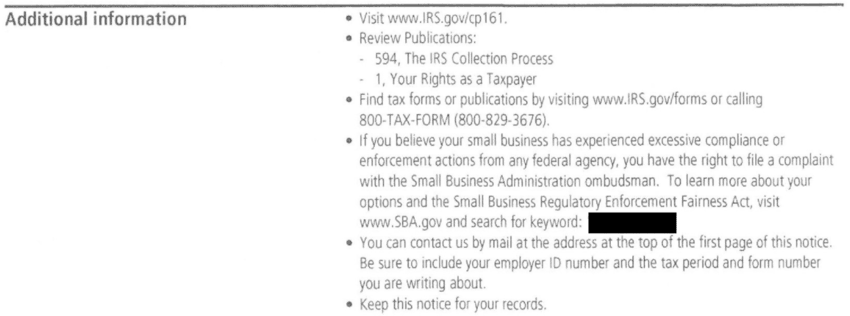

Part 6: Additional Information

Lastly, the IRS will provide you with additional information on your CP161 Notice.

As is the case for most of their notices, they will provide you with a link to their website explaining the notice a little bit more.

We’ve linked that here.

You should review your publications and ensure you know your taxpayer rights.

Additionally, if you need to, you can send them written concerns tied to the notice or your account.

Free Consultation

Got a CP161 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhat You Should Do If You Receive a CP161

Below are steps for you to take after you receive a CP161 Notice from the IRS.

Step 1: Confirm You Actually Owe The IRS

The IRS makes mistakes.

This should not be a surprise.

However, that means that the first step you should take is to ensure you actually have an outstanding balance.

The IRS is claiming you owe them money.

Is that true?

Do you owe them money, or have they not received or processed your payment?

The IRS is saying you have penalty fees you owe them.

Is that true?

Did you follow their written advice and get charged anyway?

So, check and double-check your CP161 Notice closely.

Check where they’re claiming penalties and charging you interest.

Step 1a: Dispute the Charges if the IRS is Wrong

If you are certain you found an error within your CP161 Notice, contact the IRS with the provided phone number and tell them where they’ve made an error.

You’ll need to do so within 10 days of the notice date.

Unfortunately, the likelihood of a single phone call resolving the whole situation is highly unlikely.

You’ll most likely have to call them multiple times, constantly telling your story until something happens.

You have the right to take these actions, even if it’s highly difficult.

We will do this on behalf of our client because you should not pay the IRS for charges you do not owe.

Step 2: If You Can Pay In Full, Do So

You will have 30 days from the date of the notice to pay off your balance, lest you incur more penalties and charges on your balance.

If you need to dispute some of the charges with the IRS, go through and do so.

It needs to happen sooner rather than later.

Obviously, the easiest and straightforward thing you can do is to pay off your balance in full.

It will halt all penalties from accruing and get the IRS off your back since you no longer owe them any money.

If you cannot pay, though, keep reading.

Step 3: Seek Penalty Abatement From the IRS

If you cannot pay, consider seeking penalty abatement.

Penalty abatement allows you to appeal the charges the IRS has set against you and possibly get them reduced or waived completely.

While it’s not a guaranteed solution, it’s always worth a shot to try.

Choice Tax Relief will always attempt to seek some penalty abatement for our clients.

Step 4: Seek Tax Relief

If you’ve done everything possible to plead your case with the IRS and still can’t afford your balance, consider seeking tax relief.

For some, the better option is known as an offer in compromise (OIC).

It’s an agreement between the IRS and the taxpayer (in this case, your business), allowing you to settle your debt with the IRS for less than what’s originally owed.

Unfortunately, an OIC isn’t a feasible option for everyone.

Other options like installment payments and temporary hardship placements (called currently not collectible status) help taxpayers find some relief as they work to pay off all their balances.

“They were friendly, professional, and encouraging. They helped straighten out my challenging tax situation and stuck with it until everything was resolved. I highly recommend!”

Get Help Now

Got a CP161 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.