IRS Letter LT38: What It Is and How to Respond

IRS Letter LT38 is the 2024 Reminder of Notice Resumption that the IRS’s Automated Collections System is currently sending out to remind taxpayers that:

- The IRS hasn’t forgotten about them.

- They still have a balance due with the IRS.

- While the IRS paused sending out certain collections notices such as the CP59, CP501, CP503, and CP504 in February 2022, it has now resumed sending out these collections notices and will be taken forced collections activities such as wage levies and bank garnishments if taxpayers do not deal with their tax debt.

The Letter LT38 has a deadline on it for taxpayers to pay off their balance with the IRS or otherwise enter into some kind of resolution with the government on their tax debt.

Based on what we’re seeing, this deadline is either 14 days or 21 days, depending on how large the taxpayer’s balance with the IRS is.

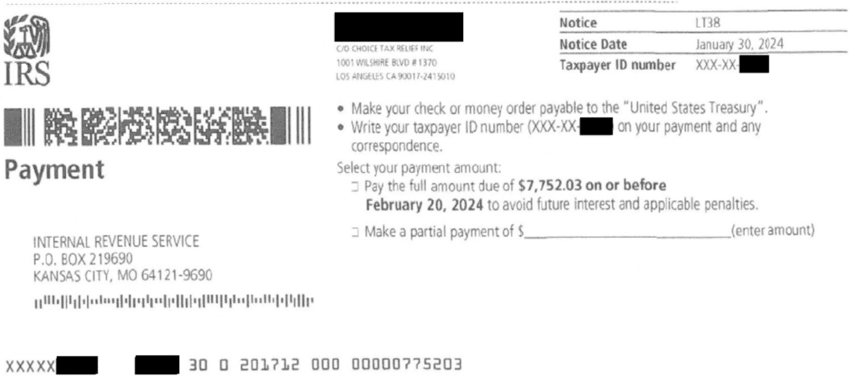

Here is a Letter LT38 that the IRS sent one of our clients with a 14-day deadline.

Here is a Letter LT38 that the IRS sent one of our clients with a 21-day deadline.

Table of Contents

IRS Letter LT38 At a Glance

| Letter Type: | Reminder |

| Generated By: | IRS ACS |

| Preceded By: | N/A |

| Followed By: | Resumption of Collections Notice Cycle |

| Recommended Action: | Pay Off Balance Due or Consider Tax Relief Options |

Why the IRS Is Sending You Letter LT38

During the COVID-19 pandemic, the IRS fell behind on collections, including sending collections notices to taxpayers with a balance due or to non-filers who have not filed a tax return.

Now, in 2024, the IRS is resuming normal collections activity, and so its automated collections division — ACS — is mailing out this LT38 Letter to taxpayers with a balance due to the IRS to remind them that the IRS is still here and has not forgotten about the taxes they owe.

The LT38 has a deadline that, if unmet, will result in the taxpayer being sent to whatever point they were in the IRS’s collections channel before the IRS paused sending out many collections notices during the pandemic.

There does not appear to be any minimum or maximum balance constraints to the LT38 Letter; we have had clients receive an LT38 for balances below $10,000 and others who received an LT38 for a very large balance.

IRS Letter LT38 Explained, Part by Part

Here is a full explanation of the Letter LT38, part by part.

Part 1: Reminder of Balance Due

On the first page of the LT38 Letter, the IRS informs the taxpayer that while during the COVID-19 pandemic the IRS suspended sending out certain collection notices, it is now “resuming normal operations” and is informing you of your balance owed, including interest and penalties.

In the box below the first paragraph, the IRS informs you of your total amount due (including interest and penalties) for all tax years with the date to which these interest and penalties were calculated to arrive at the amount indicated — this date is also the due date on the payment coupon found later in the notice.

Part 2: How to Pay Your Balance Online

Naturally, the IRS is sending you this letter with the end goal of you paying them the money you owe them, so at the bottom of page 1, the IRS informs you how you can pay your balance online at irs.gov/payments or by paper mail using the payment coupon at the end of the LT38.

Part 3: IRS Online Account Information

At the top of the second page of the LT38 Letter, the IRS tells you the things you can do with your IRS Online Account, including:

- Seeing the amount owed by year

- Seeing the dates and amounts of your payments to the IRS

- Accessing your tax records, such as transcripts

- Opting to go paperless for certain tax notices from the IRS

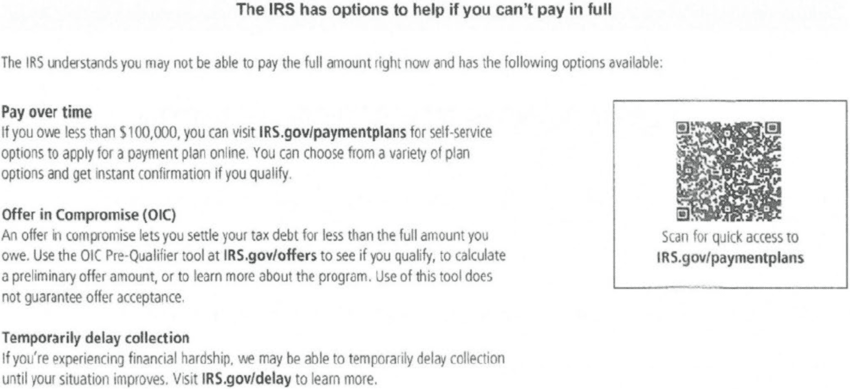

Part 4: Options If You Can’t Pay in Full

At the bottom of Page 2, the Letter LT38 breaks down — briefly — your options if you can’t pay your balance in full by the deadline.

These tax relief options include:

- Installment Agreement: An installment agreement is an agreement with the IRS to pay your tax debt over time. Obviously, the IRS wants to be paid as quickly as possible, but longer term lengths can be negotiated.

- Offer in Compromise: An offer in compromise is an agreement with the IRS to settle your tax debt for less than you owe in a lump sum paid within five or 24 months.

- Currently Not Collectible (CNC) Status: CNC status, also known as the IRS hardship program, is an agreement with the IRS during which the government will not expect you to make payments to them and will not take forced collection activity — such as a wage garnishment, bank levy, or Social Security levy — against you.

Part 5: Billing Summary

At the top of the third page, the Letter LT38 provides your billing summary, breaking down by tax period your assessed balance, your accrued interest and penalties, and finally the total.

Part 6: Automatic Penalty Relief for Certain Penalties

In December 2023, the IRS announced in Notice 2024-7 that it would be automatically granting penalty relief for certain failure-to-pay penalties for tax years 2020 and 2021.

Please watch the video below if you incurred failure-to-pay penalties for tax years 2020 and 2021 and want to learn more about this automatic penalty relief.

Part 7: More Information About Penalties and Interest

Next, the IRS tells you where you can learn more about how the IRS calculates penalties and interest as well as provides the IRS’s statutory authority for charging interest and assessing the failure-to-pay and failure-to-file penalties.

Interest

The IRS charges interest — compounded daily — on your unpaid balance.

The interest rate, which is re-evaluated and potentially adjusted quarterly, is currently 8%.

Read this article to learn more about how the IRS calculates its interest rate on underpayments.

Failure-to-Pay Penalty

The failure-to-pay penalty is a penalty that the IRS charges taxpayers who fail to pay their taxes for the year by their due date — typically April 15 of the following year.

The failure-to-pay penalty is equal to 0.5% of the unpaid tax amount per month or part of the month the taxes are unpaid, up to a maximum 25% penalty.

Note that if a taxpayer is liable for both the failure-to-file penalty and the failure-to-pay penalty for a given month, the IRS reduces the failure-to-file penalty for that month by the amount of the failure-to-pay penalty.

Failure-to-File Penalty

The failure-to-file penalty is equal to five percent of the tax amount due per month or part of a month you failed to file your return after its deadline (up to a maximum of 25%).

Part 8: Information for Joint Filers

![]()

In this short paragraph, the IRS informs joint filers that the IRS will send the same LT38 Letter to both spouses.

Part 9: Where to Find More Information

In the middle of page three, the LT38 LEtter includes some additional information for you, such as:

- The official IRS webpage for the CP22E Notice

- Where you can obtains tax forms, instructions, and publications

- How to contact the IRS

Part 10: Taxpayer Rights and Sources for Assistance

In this section, the IRS provides you with some information about the Taxpayer Bill of Rights, IRS Publication 1, Low-Income Taxpayer Clinics (LITC), and the Taxpayer Advocate Service.

Part 11: Payment Coupon

At the bottom of the last page of the LT38 Letter is the payment coupon that you would submit with your payment if you intend to pay the amount on the notice in full or in part via paper mail.

Free Consultation

Got a LT38 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhat You Should Do If You Receive an LT38 Letter

Below are the steps you should take after you receive an LT38 Letter.

For more information about each of these steps, check out our article How to Fight the IRS and Win.

Step 1: Check the LT38 Letter for accuracy.

Don’t assume that the IRS did their math correctly — review the IRS’s numbers against your own.

Step 2: Correct any errors with the IRS.

If you do find an error in the IRS’s math, take it up with them.

There should be phone numbers in the LT38 Letter itself that you can call to discuss your disagreement with the IRS’s numbers:

- For example, in the “What you need to do immediately” section, there will likely be a phone number that you can call to “discuss your options.” If you disagree with the tax amount itself, call this number.

- In the “Penalties” section, there should be a number indicated that you can call to obtain a “detailed calculation of your penalty charges.” If you disagree with the IRS’s penalty calculation, call this number.

You can always reach out to us at at 866-8000-TAX to go to bat against the IRS for you.

Step 3: Seek Penalty Abatement.

For most of our clients with penalties on their account, we at least seek some sort of penalty relief for them.

Sometimes the IRS grants it; sometimes they don’t.

But it’s generally at least worth a shot.

For more information about seeking abatement for the penalties on your account, check out this article.

Step 4: Pay the Balance Due OR Seek Tax Relief

Finally, you have to figure out what to do with the amount you owe the IRS after you’ve cleared up any disagreements with them concerning the amount as well as obtained any possible penalty relief for your account.

You can, of course, pay off your balance in full.

This will (obviously) stop future penalties and interest from accruing.

However, a better option — if you qualify for it — is an offer in compromise.

An offer in compromise is an agreement you make with the IRS in which the IRS agrees to accept a lower amount to satisfy your tax debt than you actually owe.

That said, not all taxpayers qualify for an offer in compromise, so there are other options, such as a temporary hardship placement called currently not collectible status as well as installment agreements for taxpayers who wish to pay their balance over time.

For an overview of how tax relief works, read our article What Is Tax Relief and How Does It Work?.

“I interacted with 4 other providers before finding Choice Tax Relief. All the others were offering a “let’s get your money up front, then see how this all plays out for you” approach.”

Get Help Now

Got a LT38 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.