IRS Notice CP504B: What It Is and How to Respond

IRS Notice CP504B is the Notice of Intent to Levy that is typically sent to businesses. A levy is when the IRS takes an individual’s or business’ stuff — such as money in their bank account — to satisfy their federal tax debt.

The Notice CP504B is the IRS giving your business notice that it intends to take forced collections action against your business. The CP504B is typically sent about ten weeks after the CP161 Notice and, if not responded to within about 10 weeks, typically precedes the LT11B Notice.

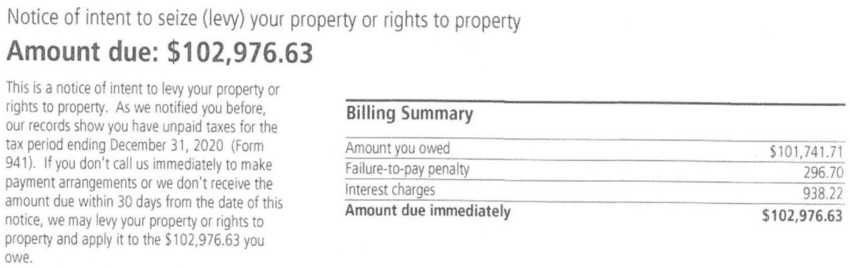

Here is a sample CP504B Notice the IRS sent to one of our clients.

The CP504B is the notice described in Internal Revenue Code § 6331(d), which requires the IRS — no less than 30 days before a levy — to send taxpayers a notice of its intent to levy the taxpayer that describes “in simple and nontechnical terms”:

- The IRS’s rules about levy and seizure of property

- The appeals and payment alternatives, or other solutions, available to you to prevent a levy

- The IRS’s rules about the certification of seriously delinquent tax debt to the State Department under Section 32101 of the FAST Act

After sending the CP504B Notice, the IRS can levy certain things. For example, under Internal Revenue Code § 6330(f)(3), if the IRS has served a levy on a state — like California, New York, Florida or Texas — through the State Income Tax Levy Program, the IRS can levy your state tax refund to be applied toward your federal tax debt after it has issued you the CP504B.

However, when it comes to other levies, such as bank levies, the IRS cannot perform those levies until it has sent you an additional notice, your Final Notice of Intent to Levy and Your Right to a Hearing, which is typically found on the LT11B Notice, which is generally sent ten or so weeks after the CP504B.

If the IRS levies you without sending you the CP504B or an equivalent notice of intent to levy — as well as the CP161 or an equivalent notice and demand, and the LT11B or an equivalent Final Notice of Intent to Levy and Your Right to a Hearing — you should contest the levy due to its improper nature.

Note, of course, that the IRS may be sending you notices at an old address!

Table of Contents

IRS Notice CP504B At a Glance

| Notice Type: | Collections |

| Generated By: | IRS ACS |

| Preceded By: | Notice CP161 |

| Followed By: | Notice LT11B |

| Recommended Action: | Enter Into Resolution |

IRS Notice CP504B Explained, Part by Part

Here is a full explanation of the Notice CP504B, part by part.

Part 1: Amount Due and Billing Summary

On the first page of the CP504B Notice, the IRS gives a line-by-line summary of what they believe your business owes.

Here, it shows the underlying amount owed, any penalties and interest you’ve been charged, any payments you’ve made for this period, and the total amount due.

To the left of the billing summary, the IRS informs you that it intends to levy your property or property rights, as well as tell you which tax period the outstanding tax is for.

You will have 30 days from the date of the notice to take action on your outstanding balance; otherwise, the IRS will take further action against you that could culminate in levies.

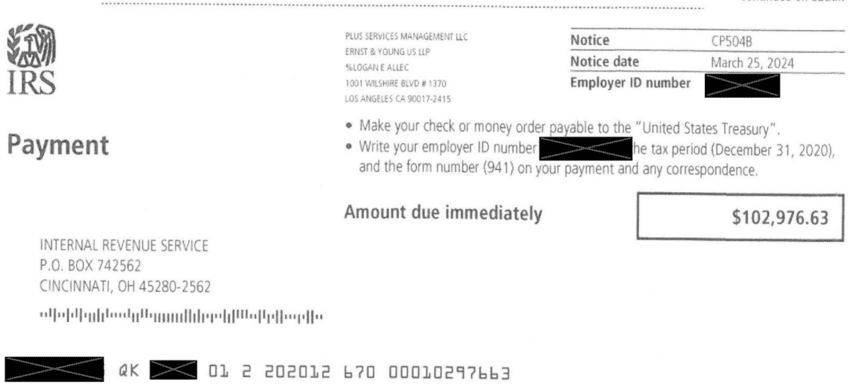

Part 2: What the IRS Wants You to Do

Next, the IRS will give you a payment coupon to pay off your balance in full via a check or money order.

If you choose to use this method of payment, then be sure to include your EIN, the tax period, and the tax return form number on the payment or correspondence.

The payment coupon is for checks and money orders. When you write a check or money order, make sure it is payable to the United States Treasury.

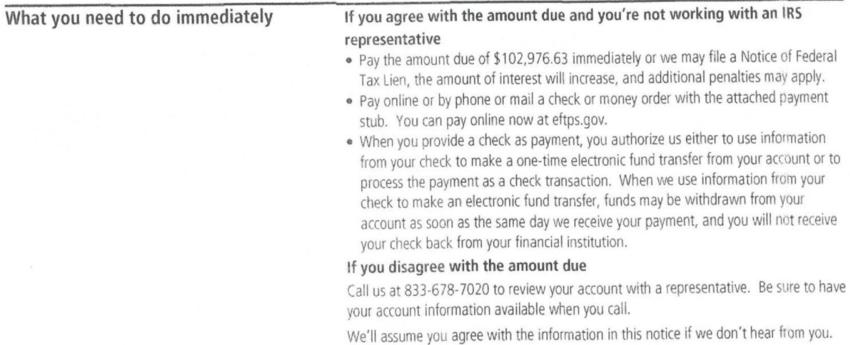

Part 3: What the IRS Wants You To Do Immediately

Next, the IRS will tell you what you need to do immediately.

Obviously, the IRS wants you to pay off your balance as soon as possible, and if you don’t, you may end up under threat of levy.

You can pay via the previously discussed payment coupon, online on the IRS website, or over the phone.

If you don’t agree with the amount due, then you can call the IRS to review your account with a representative. You must have all of your information available when you call. If the IRS doesn’t hear from you, then it will assume you agree with the balance.

Also, if you truly cannot afford to pay what you owe, you may qualify for one of several tax relief options — more on this later.

Part 4: What The IRS Needs You To Know

Next, the IRS will inform you of some important information.

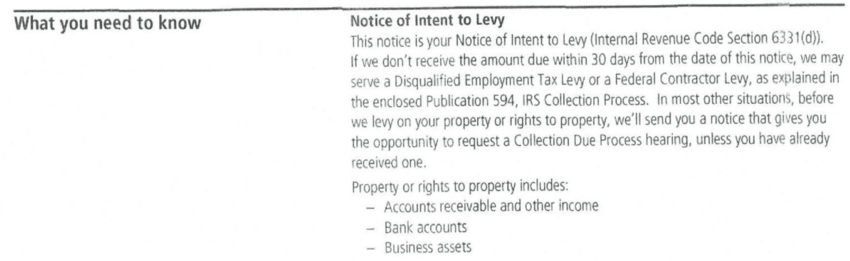

Notice of Intent to Levy

The first piece of information indicated here is that this CP504B Notice is, in fact, the notice of the intent to levy the IRS is required under IRC Section 6331(d) to send you before it takes levy action against you, meaning it can seize things like but not limited to:

- Your accounts receivable and other income

- Your bank accounts

- Your other business assets

Note that before the IRS can actually start seizing these things, it is generally required to send you a notice informing you of your right to a Collection Due Process (CDP) hearing; if you haven’t yet received this notice (such as Notice LT11B) for the tax period(s) for which you owe, the IRS can’t levy these things until it sends you one.

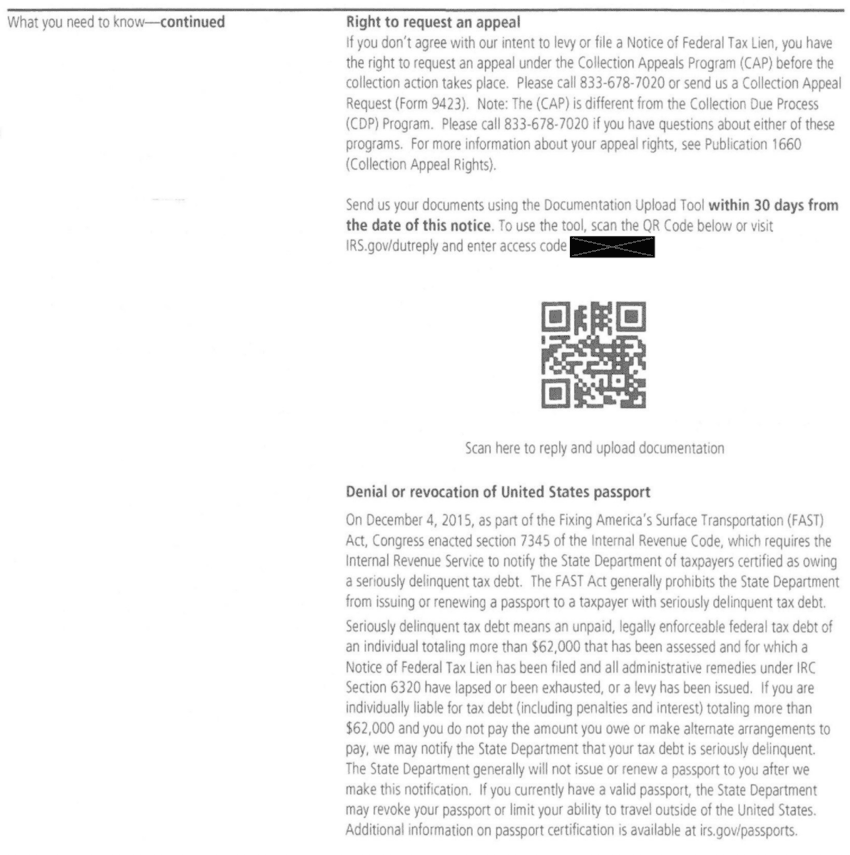

Your CAP Appeal Rights

If you do not agree with the intent to levy, you have the right to request an appeal under the Collection Appeals Program (CAP).

You will need to follow the provided instructions for the appeal process.

Potential Passport Issues

Additionally, in cases of seriously delinquent tax debt, the IRS is required to notify the State Department.

As a result of the FAST Act, the State will prohibit you from receiving a new passport or renewing it if the IRS deems your tax debt as “seriously delinquent.”

Part 5: Payment Options

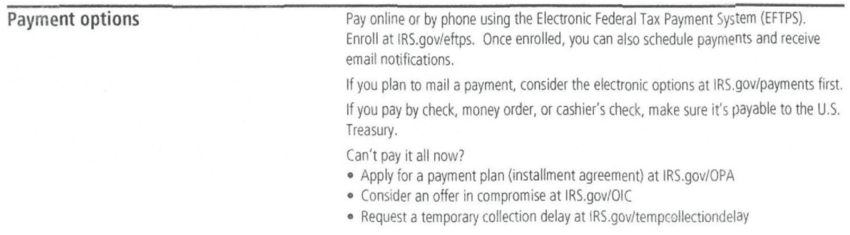

Next, the IRS will then give you some payment options.

You can pay online or by phone through the Electronic Federal Tax Payment System (EFTPS). This is more favorable than a mailed payment, though the IRS still accepts them.

If you cannot afford to pay off your balance in full now, consider a payment plan, offer in compromise (OIC), or a temporary delay in collection (currently not collectible status).

Part 6: If The IRS Doesn’t Hear From You

Next, the IRS will tell you what happens if they don’t hear from you.

If you do not make any payments, set up some kind of resolution for your tax debt, or request an appeal, then the IRS may file a Notice of Federal Tax Lien (NFTL) against you, which may make it difficult for you to sell or borrow against your property.

Obviously, the IRS can also levy your income and assets as well.

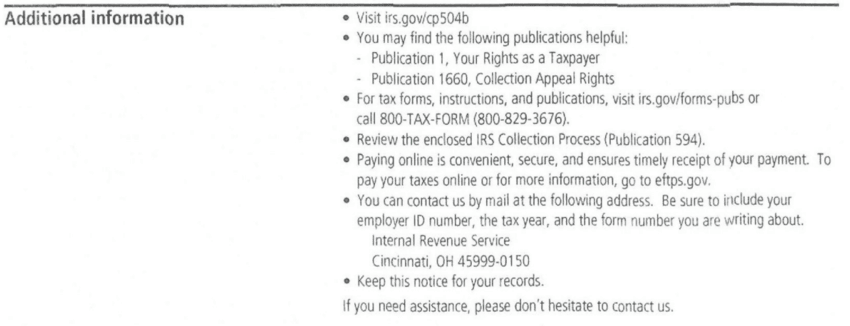

Part 7: Additional Information

Next, the IRS will give you more resources to follow through and do your own research. We’ve linked the IRS website on the CP504B here.

You can also review your taxpayer rights, the IRS collection process, or other tax forms. If you cannot find what you need online, then feel free to contact the IRS at the provided phone number.

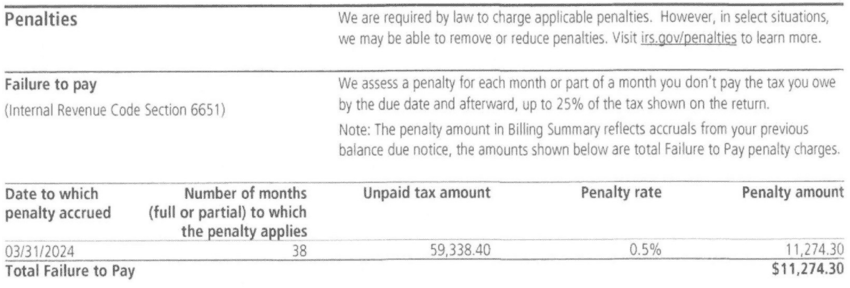

Part 8: Penalties

Then, the IRS will break down the penalties you owe them.

The penalties are calculated based on the number of months the penalty applies to, the unpaid tax amount, the penalty rate, and the penalty amount.

The IRS is required to charge penalties by law, but penalties can be appealed and removed or reduced by the IRS.

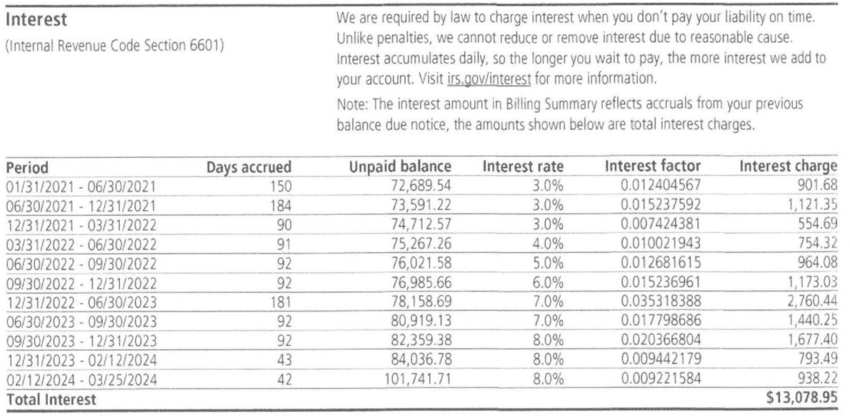

Part 9: Interest

Lastly, the IRS will provide you with a chart of interest fees.

It will have the period, the number of days accrued, the unpaid balance, interest rate, and factor, along with the interest charge and total interest.

Unlike penalties, interest cannot be removed. It also accumulates daily until the balance is paid off.

When the IRS Sends Notice CP504B

The most common reason for the IRS sending you a CP504B Notice is when the following things happened:

- Your business owed money on a previously filed tax return.

- Your business did not fully pay the amount due on the return.

- Your business previously received a CP161 Notice from the IRS, and you ignored it.

Another situation where taxpayers receive a CP504B Notice is when the IRS prepares a substitute for return (SFR) for a taxpayer and assesses the tax based on the SFR.

Alternatively, a taxpayer might have paid the balance indicated on their return when they filed it, but they incurred interest and penalties and left it unpaid.

However, the IRS is known to make mistakes, and they may be sending you the CP504B Notice in error.

What You Should Do If You Receive a CP504B Notice

Below are the steps you should take after you receive a CP504B Notice.

For more information about each of these steps, check out our article How to Fight the IRS and Win.

Step 1: Check the CP504B Notice for accuracy.

Check and double-check your CP504B notice. Review your numbers and make sure everything in your notice lines up.

Step 2: Correct any errors with the IRS.

If you do find an error in the IRS’s math, contest it with the IRS.

There should be phone numbers in the CP504B Notice itself that you can call to discuss your disagreement with the IRS’s numbers. Be prepared to tell your story multiple times and receive some pushback.

The IRS can be difficult, but we know the importance of protecting yourself from the IRS.

You can always reach out to us at 866-8000-TAX to go to bat against the IRS for you.

Step 3: Seek Penalty Abatement.

We usually try to seek penalty abatement for all of our clients.

While it’s not a guarantee that the IRS will grant it, it’s always worth trying.

For more information about seeking abatement for the penalties on your account, check out this article.

Step 4: Pay the Balance Due OR Seek Tax Relief

Lastly, you have to deal with your unpaid balance.

The most straightforward option is to pay off your balance in full. This will stop future penalties and interest from accruing.

However, if you qualify for it, an offer in compromise might be a better choice. An offer in compromise is an agreement to settle your debt for less than you owe with the IRS.

Not all taxpayers qualify for an offer in compromise, so there are other options, such as a temporary hardship placement called currently not collectible status, as well as installment agreements for taxpayers who wish to pay their balance over time.

For an overview of how tax relief works, read our article What Is Tax Relief and How Does It Work?.

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.