IRS Notice CP503: What It Is and How to Respond

IRS Notice CP503 is the 2nd Notice of a Balance Due.

It is one of the most common notices that the IRS sends out to taxpayers — it is typically sent about five weeks after the CP501 Notice and, if not responded to within about five weeks, typically precedes the CP504 Notice.

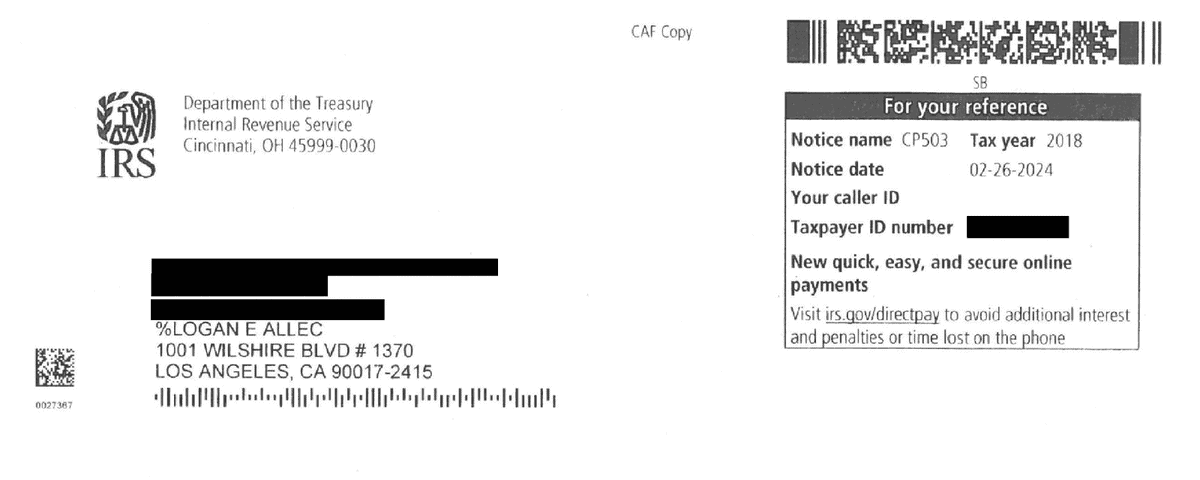

Here is a redacted CP503 Notice that one of our clients received.

Key Takeaways

- IRS Notice CP503 is the second balance-due reminder, typically sent about five weeks after the CP501 Notice.

- You generally have about 10 days (the pay-by date on the notice) to pay or make arrangements before more penalties and interest pile up.

- If your balance remains unpaid, a federal tax lien has already arisen by law — and the IRS warns it may file a public Notice of Federal Tax Lien or levy your income or bank account.

- Ignoring the CP503 Notice typically leads to the CP504 Notice — a notice of intent to levy.

- Your options include paying in full, an installment agreement, an offer in compromise, currently not collectible status, and penalty abatement.

Table of Contents

IRS Notice CP503 At a Glance

| Notice Type: | Collections |

| Generated By: | IRS ACS |

| Preceded By: | Notice CP501 |

| Followed By: | Notice CP504 |

| Recommended Action: | Enter Into Resolution |

CP501 vs. CP503 vs. CP504: What’s the Difference?

Before we dive into the CP503 Notice itself, here is how it compares to the balance-due notices that typically come before and after it.

| CP501 | CP503 | CP504 | |

|---|---|---|---|

| What it is | First balance-due reminder | Second balance-due reminder | Notice of intent to seize (levy) your property |

| When it arrives | Usually a few weeks after the CP14 Notice | About five weeks after CP501 if you don’t respond | About five weeks after CP503 if you don’t respond |

| What it warns | Pay to stop further penalties and interest | IRS may consider levying your income or bank account; a lien has arisen and an NFTL may be filed | IRS intends to levy, starting with your state tax refund |

| Urgency | Moderate | Elevated | High — enforced collection is imminent |

| Recommended action | Pay or make arrangements | Enter into resolution now | Act immediately — consider professional help |

IRS Notice CP503 Explained, Part by Part

Here is a full explanation of the Notice CP503, part by part.

Part 1: Notice Header and “For Your Reference” Box

At the top of the first page of the CP503 Notice, the IRS identifies the notice by name (CP503) in a box labeled “For your reference” along with the tax year in question, the notice date, your caller ID, and your taxpayer ID number.

Notice how the IRS now pushes taxpayers to pay online right off the bat: this box encourages you to visit irs.gov/directpay “to avoid additional interest and penalties or time lost on the phone.”

Part 2: Amount Past Due and Payment Deadline

Next, the IRS reminds you that it has already contacted you about your past-due taxes — remember, the CP503 Notice is the second balance-due notice, typically arriving after the CP501 Notice — and states your total amount past due in a large box.

Below this box, the IRS gives you a payment deadline — typically about 10 days from the notice date — to “stop further penalties and interest” and warns that if you don’t act now, it “may consider levying (seizing) your income or bank account.”

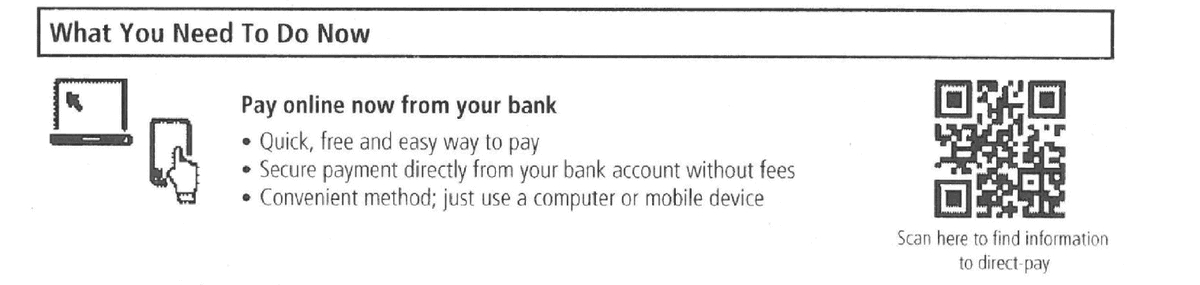

Part 3: What You Need To Do Now

In the “What You Need To Do Now” section, the IRS tells you how it wants you to pay: online, directly from your bank account, using IRS Direct Pay.

The notice even includes a QR code that you can scan with your phone to be taken directly to the IRS’s Direct Pay page.

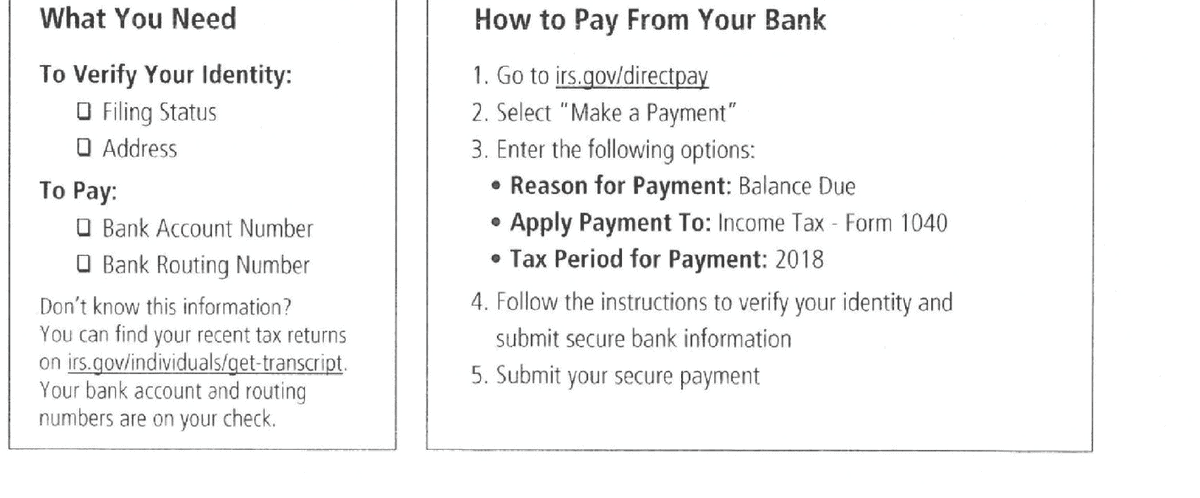

The IRS then lists what you’ll need to verify your identity (your filing status and address) and to pay (your bank account and routing numbers), followed by step-by-step instructions for submitting your payment on irs.gov/directpay.

This section continues onto the second page of the notice, where the IRS notes that if you’re a debtor in a bankruptcy case, the notice is for your information only, and that if you already paid your balance in full or set up a payment plan after receiving a previous notice, you can disregard the reminder.

It also lists a phone number to call if you can’t find what you need online and still have questions — 833-678-7020 on this client’s notice above.

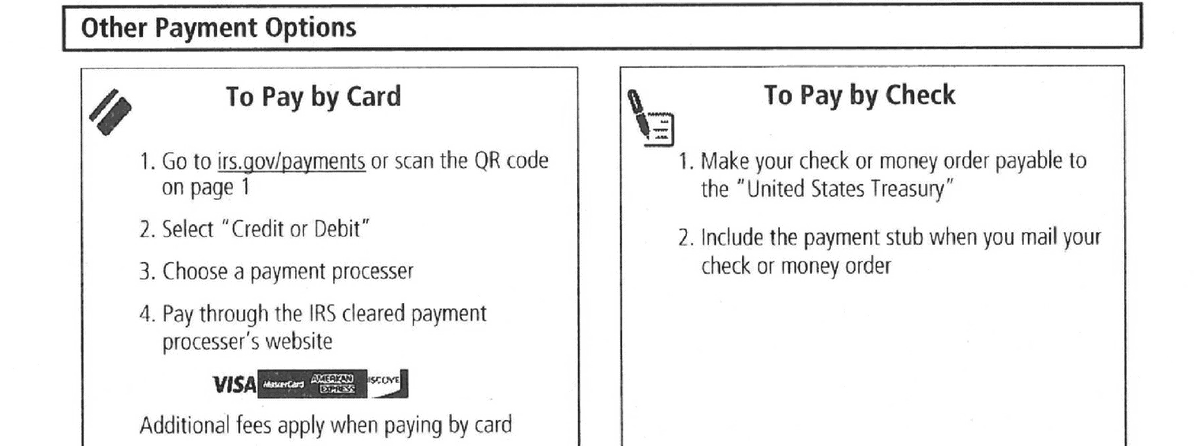

Part 4: Other Payment Options

If you don’t want to pay directly from your bank account, the IRS gives you two other ways to pay: by credit or debit card through an IRS-approved payment processor (additional processing fees apply) or by check or money order made payable to the “United States Treasury” and mailed in with the payment stub found at the bottom of the last page of the notice.

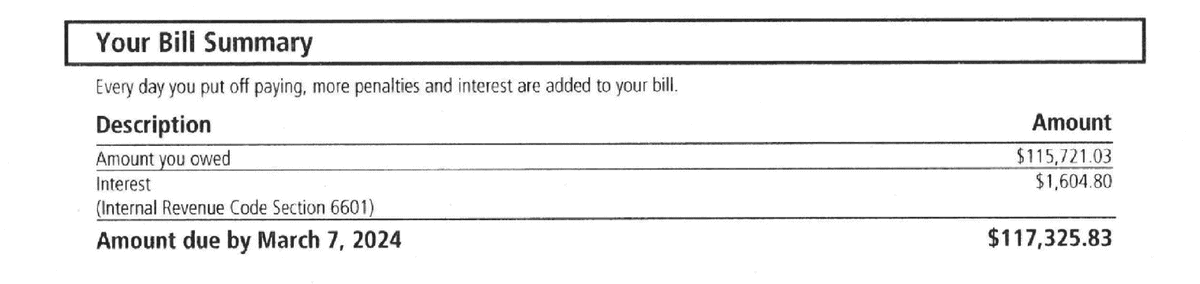

Part 5: Your Bill Summary

Next, the IRS gives a line-by-line summary of what it believes you owe.

This summary could include:

- The balance from your previous notice, indicated as the “Amount you owed” line item

- The amount of any penalties the IRS has assessed on your account — the taxpayer who received this client’s notice above did not have any penalties assessed on their account, so no penalty line items appear

- The amount of any additional interest the IRS has charged to your account

- The total amount due by your payment deadline

And right above this table, the IRS reminds you: “Every day you put off paying, more penalties and interest are added to your bill.”

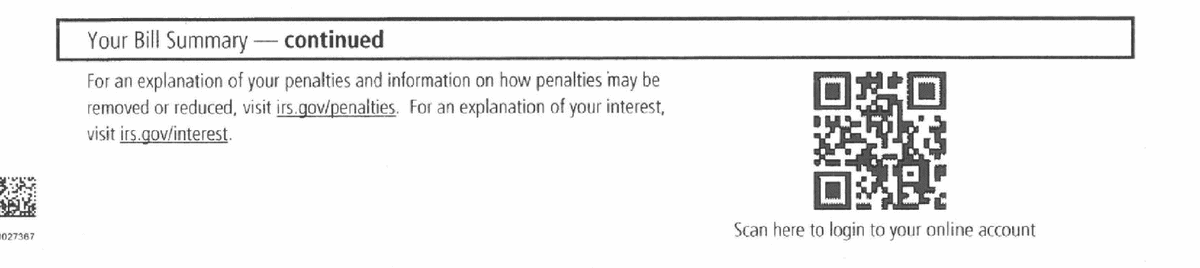

The bill summary continues on the following page, where the IRS points you to irs.gov/penalties for information on how penalties may be removed or reduced and to irs.gov/interest for an explanation of interest — along with another QR code, this one taking you to your IRS online account.

Part 6: Additional Information — Including the Federal Tax Lien Warning

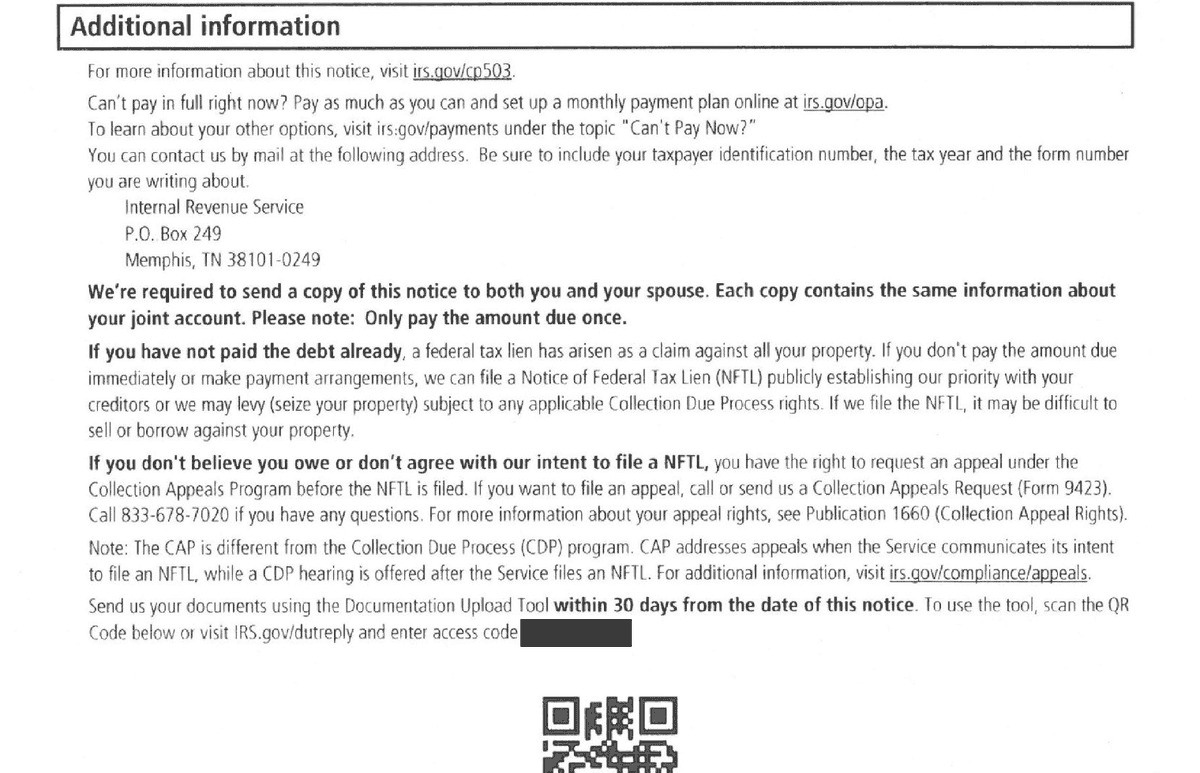

This “Additional information” section is arguably the most important part of the current CP503 Notice — and one that many taxpayers skim right past.

Here, the IRS states that if you have not paid the debt already, “a federal tax lien has arisen as a claim against all your property.”

That’s right — the lien already exists by operation of law.

The IRS then warns that if you don’t pay the amount due immediately or make payment arrangements — such as an installment agreement — it can file a Notice of Federal Tax Lien (NFTL) publicly establishing its priority with your creditors, or it may levy (seize) your property, subject to any applicable Collection Due Process rights.

The IRS also explains your appeal rights here: if you don’t believe you owe the amount or don’t agree with the IRS’s intent to file an NFTL, you have the right to request an appeal under the Collection Appeals Program (CAP) before the NFTL is filed by submitting a Collection Appeals Request (Form 9423).

Note that CAP is different from the Collection Due Process (CDP) program: CAP applies when the IRS communicates its intent to file an NFTL, while a CDP hearing is offered after the IRS files an NFTL.

Finally, this section tells you that you can set up a monthly payment plan online at irs.gov/opa, gives you the IRS mailing address to write to, and provides a QR code for the IRS Documentation Upload Tool, which you can use to send the IRS documents within 30 days of the notice date.

Part 7: Taxpayer Rights and Sources of Assistance

The IRS then describes your rights under the Taxpayer Bill of Rights and lists sources of assistance such as the Taxpayer Advocate Service (TAS) and Low Income Taxpayer Clinics (LITCs).

The notice also acknowledges that “tax professionals who are independent from the IRS may be able to help you” — which, of course, is exactly what we do here at Choice Tax Relief.

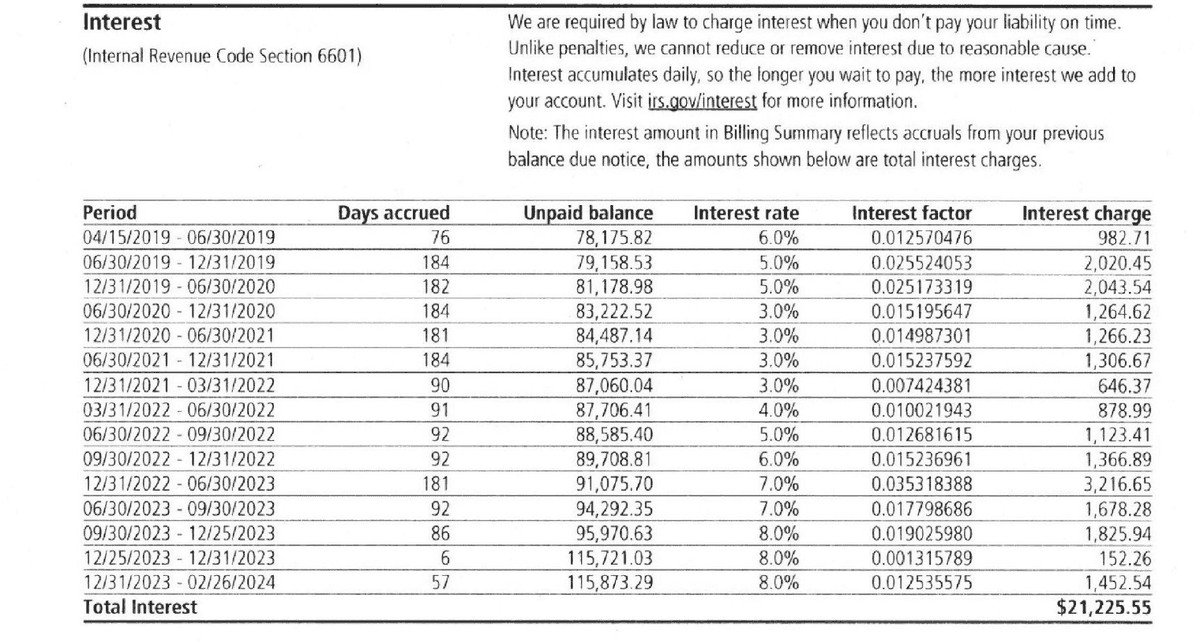

Part 8: Interest Charges Calculation

Next, the IRS breaks down the interest it has charged you, period by period, showing the days accrued, the unpaid balance, the interest rate, the interest factor, and the interest charge for each period.

Remember: interest accumulates daily, and unlike penalties, the IRS cannot reduce or remove interest due to reasonable cause.

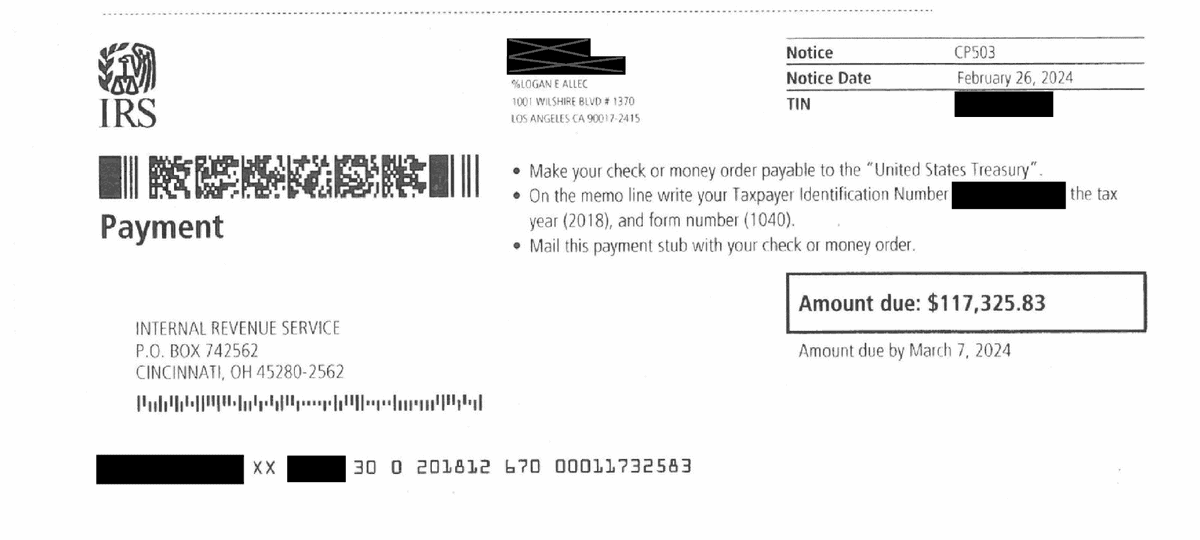

Part 9: Payment Stub

Finally, the last page of the CP503 Notice contains a payment stub to mail in with your check or money order if you pay by mail, along with your amount due, your payment deadline, and instructions for what to write on your check’s memo line.

Free Consultation

Got a CP503 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAXWhen the IRS Sends Notice CP503

The most common reason for the IRS sending you a CP503 Notice is when the following things happened:

- You filed a tax return for the year in question that indicated a balance due.

- You did not pay the amount due indicated on the return in full.

- The IRS previously sent you a CP501 Notice and you did not respond to it.

Another situation in which the IRS sends taxpayers a CP503 Notice is if the IRS itself prepared a substitute for return (SFR) for a taxpayer and the tax was assessed based on this SFR.

Or a taxpayer may have paid the balance due indicated on their return when they filed it — but they filed the return or at least paid the tax late, giving rise to penalties and interest that they have not yet paid.

Of course, the IRS is known to make mistakes, and it’s possible they are sending you the CP503 Notice in error because they didn’t properly credit your account for payments you made for the tax year.

What You Should Do If You Receive a CP503 Notice

Below are the steps you should take after you receive a CP503 Notice.

For more information about each of these steps, check out our article How to Fight the IRS and Win.

Step 1: Check the CP503 Notice for accuracy.

Don’t assume that the IRS did their math correctly — review the IRS’s numbers against your own.

Step 2: Correct any errors with the IRS.

If you do find an error in the IRS’s math, take it up with them.

The current CP503 Notice no longer lists separate phone numbers for different sections of the notice; instead, it lists one number you can call if you can’t find what you need online and still have questions not addressed in the notice — on this client’s notice above, that number is 833-678-7020.

If you disagree with the tax amount, the interest, or any penalties on the notice, call this number.

You can always reach out to us at at 866-8000-TAX to go to bat against the IRS for you.

Step 3: Seek Penalty Abatement.

For most of our clients with penalties on their account, we at least seek some sort of penalty relief for them.

Sometimes the IRS grants it; sometimes they don’t.

But it’s generally at least worth a shot.

For more information about seeking abatement for the penalties on your account, check out this article.

Step 4: Pay the Balance Due OR Seek Tax Relief

Finally, you have to figure out what to do with the amount you owe the IRS after you’ve cleared up any disagreements with them concerning the amount as well as obtained any possible penalty relief for your account.

You can, of course, pay off your balance in full.

This will (obviously) stop future penalties and interest from accruing.

However, a better option — if you qualify for it — is an offer in compromise.

An offer in compromise is an agreement you make with the IRS in which the IRS agrees to accept a lower amount to satisfy your tax debt than you actually owe.

That said, not all taxpayers qualify for an offer in compromise, so there are other options, such as a temporary hardship placement called currently not collectible status as well as installment agreements for taxpayers who wish to pay their balance over time.

For an overview of how tax relief works, read our article What Is Tax Relief and How Does It Work?.

What If I Already Paid the Amount on My CP503 Notice?

If you’ve already paid the amount indicated on your CP503 Notice, you can disregard the notice.

In fact, the IRS says on the second page of the notice:

“If you paid your balance in full, set up a payment plan after receiving a previous notice or we advised you we suspended enforced collection on your account, disregard this reminder. You can check your payment status on irs.gov/payments.”

In this case, it’s possible that the IRS had already generated the CP503 Notice before it had processed your payment.

This is not a big deal — it will simply take the IRS a few days (or even a couple weeks) to catch up.

Can the IRS “Skip” the CP503 Notice?

One of my YouTube viewers asked me if the IRS can skip the CP503 Notice and go directly from the CP501 Notice to the notice of intent to levy, such as the CP504 Notice.

The answer to this question is yes, the IRS can skip the CP503 Notice; it is not a statutorily required notice — and neither is the CP501 Notice.

In fact, we have seen cases where the IRS went directly from the CP14 Notice to the CP504 Notice!

IRS Notice CP503: Frequently Asked Questions

What is IRS Notice CP503?

IRS Notice CP503 is the second reminder the IRS sends about an unpaid tax balance. It states your amount past due, gives you a pay-by date, and warns that the IRS may consider levying your income or bank account if you don’t act.

How long do I have to respond to a CP503 Notice?

The notice gives you a specific payment deadline — typically about 10 days from the notice date — to pay in order to stop further penalties and interest. Even after that date, you can still pay or set up a payment plan, but the sooner you act, the better.

What happens if I ignore the CP503 Notice?

Penalties and interest keep accruing, and the IRS typically follows up with the CP504 Notice — a notice of intent to levy. The IRS may also file a Notice of Federal Tax Lien publicly establishing its claim against your property.

Does a CP503 Notice mean I have a tax lien?

By operation of law, a federal tax lien arises once the IRS assesses the tax, demands payment, and you don’t pay. The CP503 Notice warns that the IRS may additionally file a Notice of Federal Tax Lien (NFTL), which makes the lien public record and can affect your ability to sell or borrow against your property.

Can I set up a payment plan after receiving a CP503 Notice?

Yes. You can set up a monthly payment plan online at irs.gov/opa, or work with a tax professional to negotiate an installment agreement — or, if you qualify, an offer in compromise or currently not collectible status.

What if I already paid the amount on my CP503 Notice?

If you paid your balance in full or set up a payment plan after receiving a previous notice, the IRS says you can disregard the reminder. You can check your payment status at irs.gov/payments.

“They were friendly, professional, and encouraging. They helped straighten out my challenging tax situation and stuck with it until everything was resolved. I highly recommend!”

Get Help Now

Got a CP503 Notice? Don’t wait for the IRS’s next move.

Talk to a tax expert — free, no obligation. We’ve resolved over $20 million in IRS debt for our clients.

Call 866-8000-TAX

Author:

Logan Allec, CPA, Founder and Owner

Logan Allec has been serving taxpayers as a CPA for over 14 years. After leaving his role at a "Big 4" firm, he started Choice Tax Relief to help everyday Americans who have found themselves behind on their taxes. He also educates thousands of people daily about tax relief on his YouTube channel. In addition to his CPA license, Logan also has a Master's Degree in Taxation from the University of Southern California (USC). He lives with his wife and children in the Los Angeles area. Learn more about Logan here.